PhysicsWallah Shares Rally 18%: Why the Edtech Stock Suddenly Rebounded

PhysicsWallah backed out of direct student lending and shifted to an NBFC partnership model. Here's why investors cheered an 18% single-day surge.

PhysicsWallah shares surged nearly 18% on June 4, 2026, after the company scrapped its direct student lending plan and pivoted to NBFC partnerships, removing balance sheet and credit risk from its books. In Q4 FY26, losses fell 76% year-on-year to ₹69 crore on 51% revenue growth to ₹919 crore. For the full year, FY26 revenue rose 35% to ₹3,899 crore while annual losses narrowed 90% to just ₹24 crore.

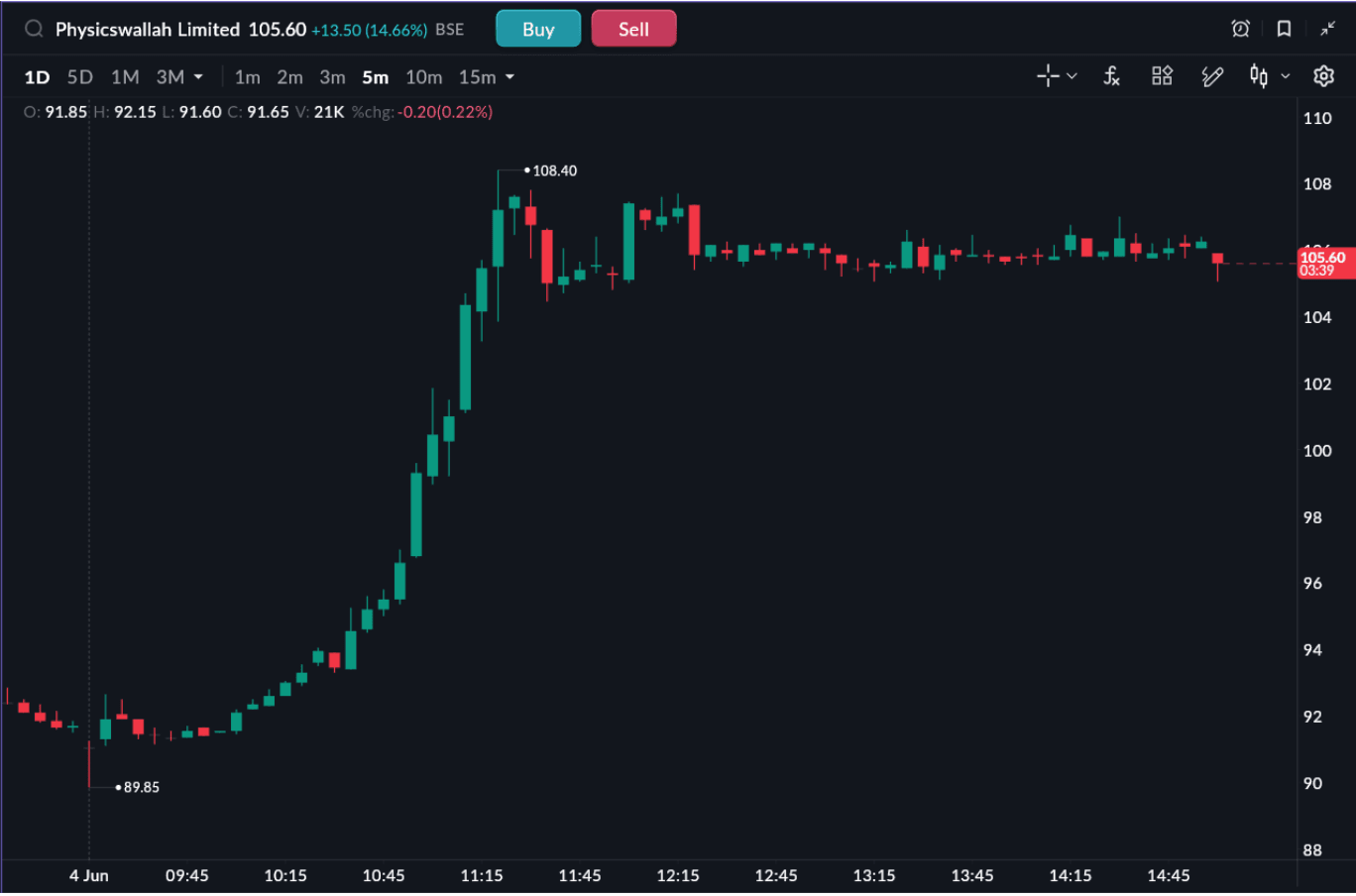

PhysicsWallah shares jumped nearly 18% on Thursday, which is its biggest single-day move in months, adding close to ₹5,000 crore to its market cap (NSE data, June 4, 2026). The stock had been falling for five straight days, and the turnaround came down to one announcement: the company was backing out of its plan to lend directly to students.

The stock hit ₹108.44 on the NSE intraday. Market cap crossed ₹31,300 crore.

The lending pivot

PhysicsWallah told the exchanges it would stop funding students through its own finance arm and would instead route loans through multiple regulated third-party NBFCs. The company called it a decision to "materially reduce balance sheet and credit-related risks." Shares responded that day.

What makes this interesting is the reversal it represents. Just last month, PW had put nearly ₹120 crore into its wholly-owned subsidiary, FinZ Finance Private Limited, as part of a broader push into student lending (PhysicsWallah exchange filing, May 2026). Now that subsidiary's future is essentially on hold, subject to board and regulatory approval. Hard to read that as anything other than the company getting the message from the market.

Why investors cared

Direct lending is a different business from running an education platform. Default risk, capital adequacy requirements, and RBI oversight, it compounds the balance sheet in ways that make investors nervous, especially in a sector that was already trying to prove it could be profitable.

By using NBFC partners instead, PhysicsWallah keeps the affordability angle for students without absorbing the credit risk itself. Whether that's the right long-term call is debatable. But it's clearly what investors wanted to hear.

The share was trading 14.66% higher as of 3:01 PM on June 4, 2026 (NSE).

What the numbers say

The broader context helps explain why investors are protective of PW's current trajectory.

In Q4 FY26, losses fell 76% year-on-year to ₹69 crore while revenue grew 51% to ₹919 crore (PhysicsWallah Q4 FY26 earnings filing). For the full year, losses came in at ₹24.17 crore versus ₹243.26 crore in FY25. Revenue from operations rose 35% to ₹3,899.54 crore, from ₹2,886.64 crore (PhysicsWallah FY26 annual report).

The offline expansion has been aggressive. PW went from 198 centers to 353 in FY26, spending around ₹250 crore in capex to get there. Faculty grew 34% to 6,837, total headcount reached 18,997, and the total student base stood at 14.2 crore (PhysicsWallah FY26 annual report).

That is a company executing on its core model. The lending detour, brief as it turned out to be, was seen as a distraction from that.

The bigger read

Markets have been less forgiving of balance sheet risk since the Byju's collapse made edtech debt a genuine cautionary tale in India. PhysicsWallah knows this. Its pivot away from direct lending isn't just financially sensible, it's also reputationally clean.

Whether the NBFC partnership model delivers as much value long-term as running lending in-house might have, nobody knows yet. But right now, "less risky and still growing" is a story this market will bid up.