IEX Shares Fall 7%: What Is Market Coupling and Why Does It Threaten IEX's Business?

CERC's market coupling draft removes IEX's price discovery advantage. Here's the full timeline, what changes, who wins, and what IEX investors need to know before Q4 results on April 23.

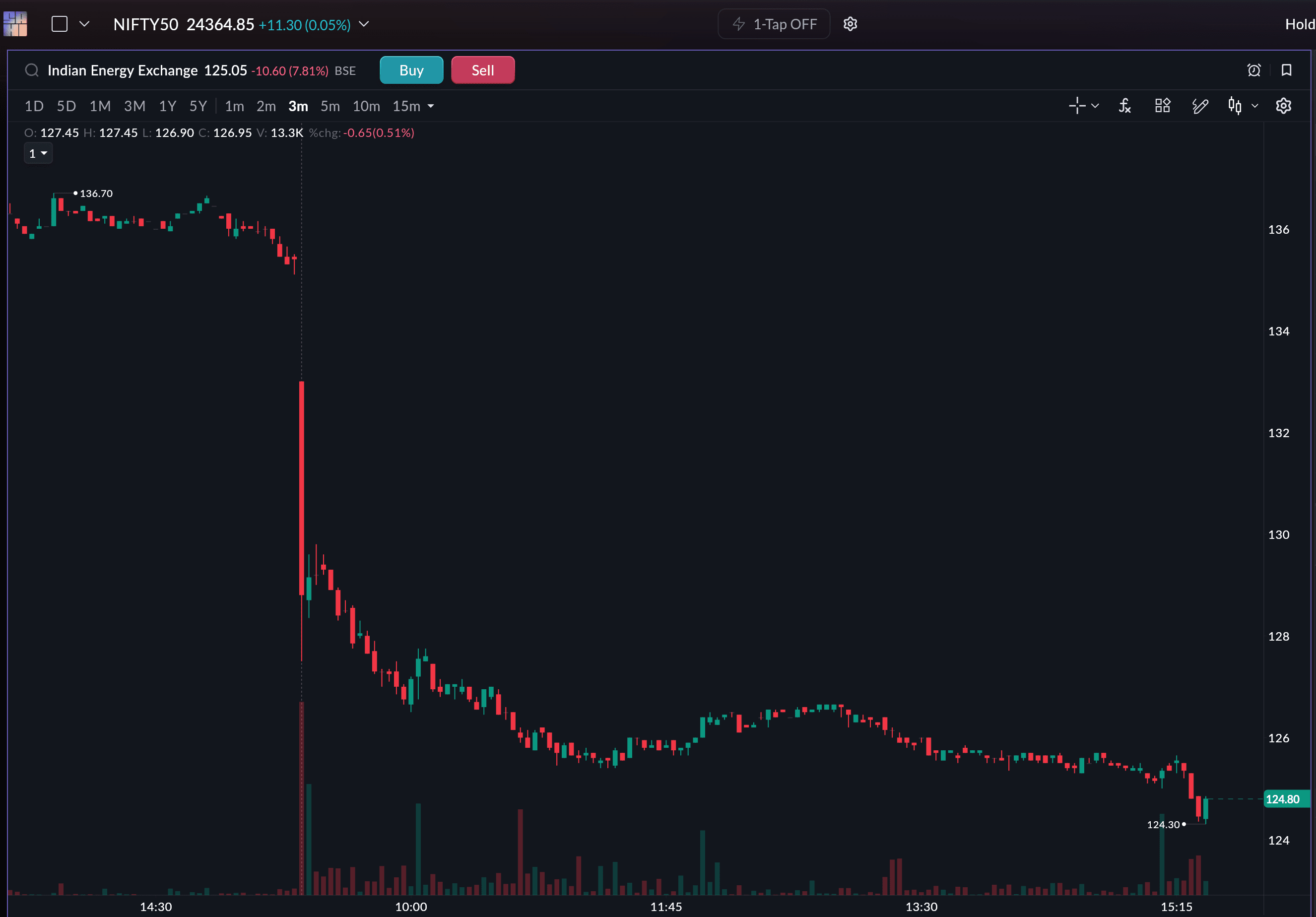

IEX Share Price Fall — Market Coupling Explained: Shares of Indian Energy Exchange (IEX) fell as much as 7.5% on April 20, 2026, after CERC released a draft notification proposing a market coupling framework for India's power exchanges. Under the proposed system, Grid India will act as a central Market Coupling Operator, aggregating all bids from all exchanges and determining one uniform electricity price — replacing IEX's current role as the primary price discovery mechanism. IEX holds approximately 85% of India's exchange-based electricity trading market. If implemented, market coupling could significantly erode this dominance. APTEL dismissed IEX's legal challenge in February 2026. Stakeholder feedback is due by May 16, 2026. IEX Q4 FY26 results are scheduled for April 23, 2026.

April 20, 2026, started badly for anyone holding IEX shares. By mid-morning, the stock was down as much as 7.5%, touching a low of ₹124.30. The culprit? A draft notification from the Central Electricity Regulatory Commission (CERC) about something called "market coupling." (Share price as of 20th April)

(Share price as of 20th April)

If you're wondering what market coupling is and why it matters, you're not alone. But here's the thing — this isn't just another regulatory update. It's a complete reimagining of how India trades electricity. And it could fundamentally alter IEX's future.

First, What Does IEX Actually Do?

Think of IEX as the stock exchange for electricity, except instead of shares, people trade megawatt-hours of power.

The Indian Energy Exchange operates through a double-sided closed auction process where state electricity boards, power-producing companies, transmission companies, and power traders can buy and sell energy. It's not a place for retail investors. To trade on IEX, you need at least ₹150 lakh in capital and clearances from the Central Electricity Regulatory Commission.

IEX started operations in 2008 and quickly became the dominant player. Today, IEX holds approximately 85% of the exchange-based electricity trading market and nearly 99% in the Day-Ahead Market and Real-Time Market. That's not just market leadership — that's near-monopoly territory.

IEX makes money primarily through transaction fees. Every unit of electricity traded on its platform generates revenue. The more electricity flows through IEX, the more money it makes. Simple business model.

But what made IEX truly special wasn't just facilitating trades. It was discovering prices.

The Magic of Price Discovery

In electricity markets, price discovery is everything. When a distribution company in Bangalore needs extra power for tomorrow afternoon, what should it pay? When a private generator in Gujarat has surplus capacity, what price can it get?

Currently, IEX answers these questions. Buyers and sellers submit their bids to IEX. The exchange runs its matching algorithm and determines a market-clearing price — the point where supply meets demand.

This created a powerful network effect. Because IEX had the most buyers and sellers, it had the deepest liquidity. Because it had deep liquidity, it discovered the most accurate prices. Because it discovered accurate prices, more participants joined IEX instead of competitors like Power Exchange India Limited (PXIL) or Hindustan Power Exchange (HPX). The smaller exchanges were stuck in a catch-22, even if buyers were ready to pay premium prices or sellers wanted to offer lower prices on PXIL, they couldn't find enough counterparties because most market participants were already on IEX.

This dominance translated into serious pricing power. IEX could charge transaction fees without worrying too much about competition. Where else would participants go? It's the same dynamic that makes tracking institutional participation in a market so useful — concentrated activity tells you where the real advantage lies.

Enter Market Coupling

Market coupling changes the game entirely.

Under the proposed system, Grid India will act as the Market Coupling Operator (MCO), aggregating bids from all exchanges and determining a uniform market clearing price for the entire country.

Currently, if you submit a bid to IEX and someone else submits a bid to PXIL, you're participating in two separate auctions with two different prices. Under market coupling, all bids from all exchanges go into one central pool. Grid India runs a single algorithm and produces one national price.

Suddenly, IEX doesn't control price discovery anymore. Grid India does.

And here's the consequence. If the price is the same everywhere, there's little incentive to prefer IEX over other platforms. It's the equivalent of all e-commerce platforms being forced to sell at identical prices — Amazon's convenience advantage shrinks dramatically. You might as well buy from Flipkart.

| Feature | Current System | Under Market Coupling |

|---|---|---|

| Price discovery | Each exchange independently | Central MCO (Grid India) |

| Clearing price | Different across exchanges | Single uniform national price |

| IEX's role | Bid collection + price discovery | Bid collection only |

| Competitive advantage | IEX has dominant liquidity edge | Level playing field across exchanges |

| PXIL/HPX ability to compete | Severely limited | Significantly improved |

Source: CERC draft notification, April 2026

The Implementation Timeline

This isn't hypothetical. Under the phased rollout originally proposed in July 2025, the Day-Ahead Market was targeted to transition to a round-robin market coupling model. The current April 2026 draft notification is the formal regulation-making step, CERC is now codifying the framework into law.

The draft states that Grid India, with the approval of the Commission, will formulate the Power Market Coupling Procedure (PMCP) within six months of the notification of amendments. CERC has invited feedback from stakeholders by May 16, 2026.

The Day-Ahead Market is IEX's bread and butter — it holds a 98.8% market share in this segment and it contributes over 81% of IEX's total trading volumes. Losing control of price discovery here is like Google losing control of its search ranking algorithm. The entire competitive advantage evaporates.

Not IEX's First Rodeo

Today's sell-off wasn't unprecedented. Here's the full timeline of this regulatory battle:

| Date | Event | IEX Stock Reaction |

|---|---|---|

| July 23, 2025 | CERC issued final order for phased market coupling rollout | Crashed ~30% the following session |

| Aug–Nov 2025 | IEX challenged CERC order at APTEL; tribunal admitted appeal, added PXIL and HPX as respondents | Partial recovery; cautious sentiment |

| January 6, 2026 | APTEL made strong observations questioning CERC's regulatory process | Surged over 9% |

| February 13, 2026 | APTEL dismissed IEX's petition, allowing CERC to proceed | Fell over 5% |

| April 20, 2026 | CERC released formal draft notification with market coupling framework | Fell up to 7.5% |

Source: BSE/NSE exchange filings; Multibagg AI; Business Today, compiled April 2026

The legal battle is over. APTEL dismissed IEX's petition in February 2026. Market coupling is happening. Today's draft is the formal regulation-making step that makes implementation real.

What This Means for IEX's Business

Analysts predict IEX's market share could drop from approximately 85% today to around 50% by FY28. That's not a haircut — that's a fundamental reset of the business.

The revenue model could also compress. When you're the dominant exchange with unique pricing power, you can charge premium transaction fees. When you're one of several equal platforms competing for business, you compete on price and service. That typically means lower margins. IEX historically enjoyed high operating margins because of its scale dominance. That may change as competition intensifies.

IEX isn't standing still. The company has expanded into trading renewable energy certificates, energy saving certificates, and natural gas. But these are significantly smaller revenue contributors compared to electricity trading.

Why Regulators Want This

From CERC's perspective, market coupling makes complete sense. The stated objectives are: discovery of a uniform market clearing price, optimal use of transmission infrastructure, and maximisation of economic surplus across buyers and sellers.

Regulators also described IEX as "monopolistic" in their final APTEL affidavit and characterised IEX's legal challenge as an attempt to "preserve entrenched market power." From a policy angle, the question is legitimate: should one private company control 85% of a critical infrastructure market like electricity trading, and should price discovery for an essential commodity be concentrated in a single platform?

CERC's answer is clearly no. The intent is to democratise the market.

The Winners and Losers

IEX is the obvious loser from this structural change. Its shareholders have had a difficult year — the stock is down over 32% in the past year even before today's fall.

The winners are smaller exchanges. PXIL and HPX gain a structural equaliser that removes the barrier traders previously had about using smaller platforms. If prices are uniform across exchanges, PXIL and HPX can compete on transaction costs, service quality, and user experience — things they couldn't compete on before because liquidity was entirely on IEX's side.

Electricity consumers may also benefit over time. More competition typically drives innovation and reduces costs. India's broader energy buildout — whether solar EPC as seen with Waaree Renewable's record-breaking revenue growth or wind energy as seen with Suzlon's institutional accumulation — will only increase the volumes flowing through India's electricity markets. A more competitive trading infrastructure will matter more, not less, as that capacity comes online.

The Bigger Picture

This story is really about the limits of network effects when regulators intervene.

Network effects are powerful. They're why IEX dominated India's power exchange market for nearly two decades. The more participants you have, the more valuable your platform becomes, which attracts more participants. It's a self-reinforcing cycle — and it's very hard to break commercially.

But network effects aren't invincible, especially in regulated industries where the product being traded is an essential commodity. When regulators decide that concentrated price discovery in a single private platform is bad for the overall market, they have the tools to break the cycle, even if the existing player is efficient and well-run. That is precisely what is happening to IEX.

IEX's Q4 FY26 results are scheduled for April 23, 2026. Investors will be watching both the numbers and any management commentary on the market coupling timeline. For broader context on how India's energy sector is being reshaped simultaneously from multiple directions — thermal, renewable, and now nuclear — Adani Power's all-time high on the same day IEX was falling tells a different but connected story about India's power market transition.

Disclaimer: This article is for informational purposes only and does not constitute financial advice. Please consult a SEBI-registered advisor before making investment decisions.