Suzlon Energy FII Holding March 2026: Shareholding Pattern and Institutional Trend

Foreign Institutional Investor (FII) participation in Suzlon Energy remains a key indicator of institutional interest in India’s renewable energy sector. The March 2026 shareholding data reflects changes in ownership structure across FIIs, DIIs, and promoters.

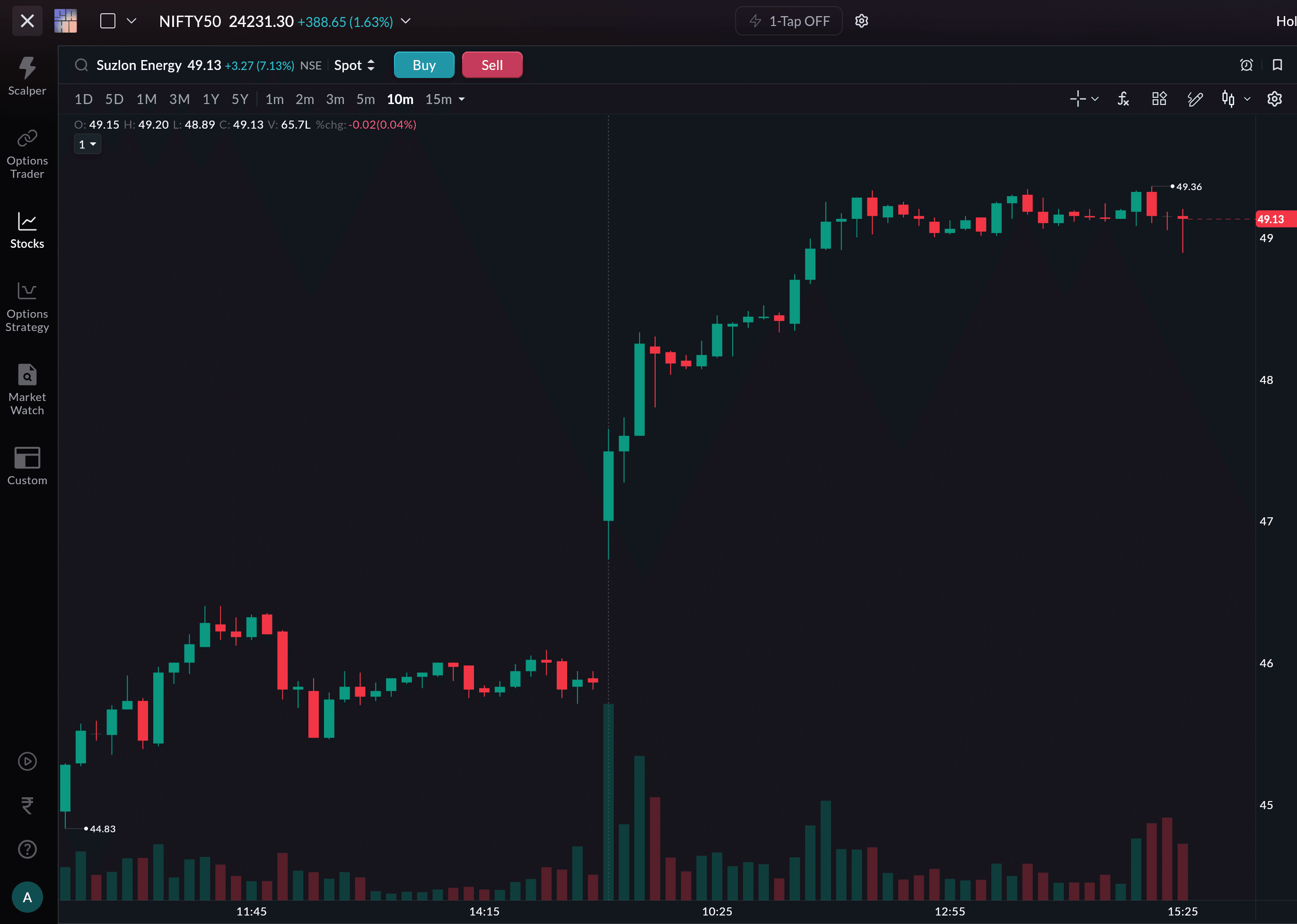

Why are FIIs buying Suzlon? Foreign institutional investors raised their stake in Suzlon Energy from 22.8% to 23.8% in Q4 FY26 — adding approximately 1.68 crore shares — even as FIIs pulled over ₹1 lakh crore out of Indian equities in the same quarter. The counter-cyclical buying reflects a long-duration bet on India's wind energy transition: India needs to add significant wind capacity to meet its 500 GW renewable target by 2030, added a record 6.05 GW in FY26 alone, and Suzlon holds approximately 30–35% of India's wind turbine installation market with a 6.4 GW order book, net cash of ₹1,556 crore, and the country's largest domestic manufacturing capacity of 4,500 MW. The stock rose over 7% on April 15, 2026, touching ₹49.34 intraday.

Here's a puzzle worth thinking about.

Foreign institutional investors spent much of the January–March 2026 quarter dumping Indian equities, over ₹1 lakh crore worth. And yet, buried in Suzlon Energy's BSE shareholding data was something that ran completely against that grain.

They were buying Suzlon.

That sent the stock surging over 7% on April 15, touching an intraday high of ₹49.36, before trading around ₹49.13, up 7.13% — with 80 million shares changing hands. Not bad for a stock that was near ₹38 just weeks ago.

So what's going on?

The Turnaround No One Wants to Forget

To understand today, you have to understand where Suzlon came from.

Founded in 1995 by Tulsi Tanti, Suzlon was once India's most celebrated wind energy story, a global giant that acquired European companies, expanded into 17 countries, and seemed unstoppable. Then it nearly fell apart. Aggressive acquisitions, ballooning debt, and a global financial crisis brought it to its knees. For years, the stock was almost synonymous with value destruction.

But through painstaking deleveraging and a sharp refocus on the domestic market, the company clawed its way back. The turnaround is visible in the numbers. By FY2025-26, Suzlon was posting full-year revenues of ₹10,993 crore and profits of ₹2,071 crore. In its most recent quarter (Q3 FY26, October–December 2025), revenue grew 42% year-on-year to ₹4,228 crore and net profit rose 15% year-on-year to ₹445 crore — with a record 617 MW of turbines delivered in that single quarter. Net cash on the books stood at ₹1,556 crore as of December 2025, and the order book hit a record high of 6.4 GW.

A company that was drowning in debt is now sitting on cash. That's the kind of turnaround that makes institutional investors pay attention.

A company that was drowning in debt is now sitting on net cash. That's the kind of turnaround that makes institutional investors pay attention.

The FII Signal — and Why It Matters

Here's the number that caught everyone's attention. Understanding how to read FII/DII data is essential context here — because the selective nature of this accumulation is precisely what makes it significant.

| Investor Category | Q3 FY26 (Dec 2025) | Q4 FY26 (Mar 2026) | Change |

|---|---|---|---|

| FII / FPI holding | 22.8% | 23.8% | +1.0 pp |

| FII shares held | — | 3.27 billion+ | +~1.68 crore shares added |

| Mutual fund holding | 4.82% | 4.87% | +0.05 pp |

| MF shares held | — | 668 million+ | Gradual accumulation |

| Promoter holding | 11.7% | 11.7% | Unchanged |

Source: BSE shareholding pattern, Q4 FY26 (March 2026); NSE data

On its own, a 1 percentage point(pp) increase in FII holding might not seem dramatic. But the context makes it remarkable. This was a quarter where FIIs were pulling money out of Indian equities at a historic pace, over ₹1 lakh crore in outflows from the broader market. And yet, someone was buying Suzlon. That kind of selective, counter-cyclical accumulation is a signal that institutional investors believe the correction in Suzlon's stock, which had fallen nearly 10–12% in calendar year 2026 at the time, represented a buying opportunity rather than a warning sign.

The Motilal Oswal Nifty India Manufacturing ETF also disclosed a fresh 1.05% stake in the March quarter, suggesting Suzlon had entered a new index, which means automatic passive buying every time that ETF grows.

The Wind at Suzlon's Back

There's a macro reason why smart money is quietly positioning itself here. India's energy transition targets create structural demand that is difficult to ignore:

| India Wind Energy Data Point | Figure | Source |

|---|---|---|

| Total installed wind capacity (as of March 2026) | 56+ GW | MNRE, April 2026 |

| Wind capacity added in FY2025-26 | 6.05 GW (highest ever; +46% YoY) | MNRE, April 6, 2026 |

| Non-fossil fuel capacity target by 2030 | 500 GW | Government of India |

| Suzlon's domestic installed capacity managed | 15.4+ GW across India | Suzlon company data |

| Suzlon's domestic wind market share | ~30–35% of annual installations | Analyst estimates; company guidance |

| Suzlon's domestic manufacturing capacity | 4,500 MW per annum | Suzlon Q3 FY26 results |

| Suzlon's current order book | 6.4 GW (record, as of Dec 2025) | Suzlon Q3 FY26 results |

| S144 turbine share of order book | ~90% | Suzlon Q2 FY26 results |

Source: MNRE press release April 2026; Suzlon Q2 and Q3 FY26 exchange filings

India just recorded its highest-ever annual wind capacity addition of 6.05 GW in FY26 — a 46% jump over FY25 and a new national record, surpassing the previous high of 5.5 GW set in FY2016-17, per the Ministry of New and Renewable Energy. Someone has to make those turbines.

Through its OMS (Operations and Maintenance Services) division, Suzlon also earns recurring, long-term maintenance revenue from thousands of turbines already spinning across the country — with OMS margins running at approximately 40%. That's a recurring annuity income stream layered on top of the project business.

Under what the company is now calling "Suzlon 2.0," management has articulated an ambition to become a full-stack clean energy solutions company, spanning wind, solar, storage, and green hydrogen. It's no longer just a turbine maker.

The Risk Worth Watching

None of this means the story is without risk. The Q3 FY26 net profit figure illustrates the lumpiness of the business clearly:

| Quarter | Revenue | PAT | Sequential PAT Change |

|---|---|---|---|

| Q1 FY26 (Apr–Jun 2025) | ₹3,117 crore | ₹324 crore | — |

| Q2 FY26 (Jul–Sep 2025) | ₹3,866 crore | ₹1,279 crore* | +295% QoQ |

| Q3 FY26 (Oct–Dec 2025) | ₹4,228 crore | ₹445 crore | −65.2% QoQ |

Source: Suzlon Energy quarterly results, BSE filings. *Q2 PAT includes ₹718 crore deferred tax asset recognition — underlying profit was significantly lower.

The Q2 PAT of ₹1,279 crore was inflated by a one-off deferred tax asset recognition of ₹718 crore. Strip that out and the underlying profit was closer to ₹561 crore. The Q3 drop to ₹445 crore, while optically sharp, reflects normalisation rather than operational deterioration — but it's a reminder that earnings visibility in this business is lumpy. Project delivery cycles don't land in smooth, predictable instalments.

The stock is also still down about 10–12% in calendar year 2026 despite today's bounce. The 52-week high of ₹74.30 feels distant. And the broader market environment for FII flows remains uncertain — a further bout of risk aversion globally could see even patient FII positions get unwound.

The Bigger Picture

Here's what today's 7% move is really telling you.

When foreign investors quietly buy a stock during a period of broad market selling, they're not making a short-term trade. They're making a long-duration bet. FIIs vs DIIs — how institutional flows impact Indian markets explains why this kind of counter-cyclical accumulation is one of the more reliable signals to track.

The bet they appear to be making on Suzlon is this: India's energy transition is irreversible, the government has both the will and the policy machinery to push it forward, and Suzlon — with its market share, manufacturing capacity, and reformed balance sheet — is one of the best-positioned companies to ride that wave.

The stock has already proved it can go from near-zero to a multibagger once. The FIIs who missed that first leg appear to be building their positions quietly before the next one. Whether they're right is, of course, the billion-rupee question. But the signal is hard to ignore.

Disclaimer: This article is for informational purposes only and does not constitute financial advice. Stock prices and shareholding data cited are as of April 15, 2026. Analyst targets are for informational reference only. Please consult a SEBI-registered financial advisor before making any investment decisions.