Why PSU Bank Stocks Are Falling: War, Bond Yields & Market Pressure Explained

PSU bank stocks fell over 3.86% on March 27 — here's why crude, bond yields, the rupee, and fiscal concerns all hit at once.

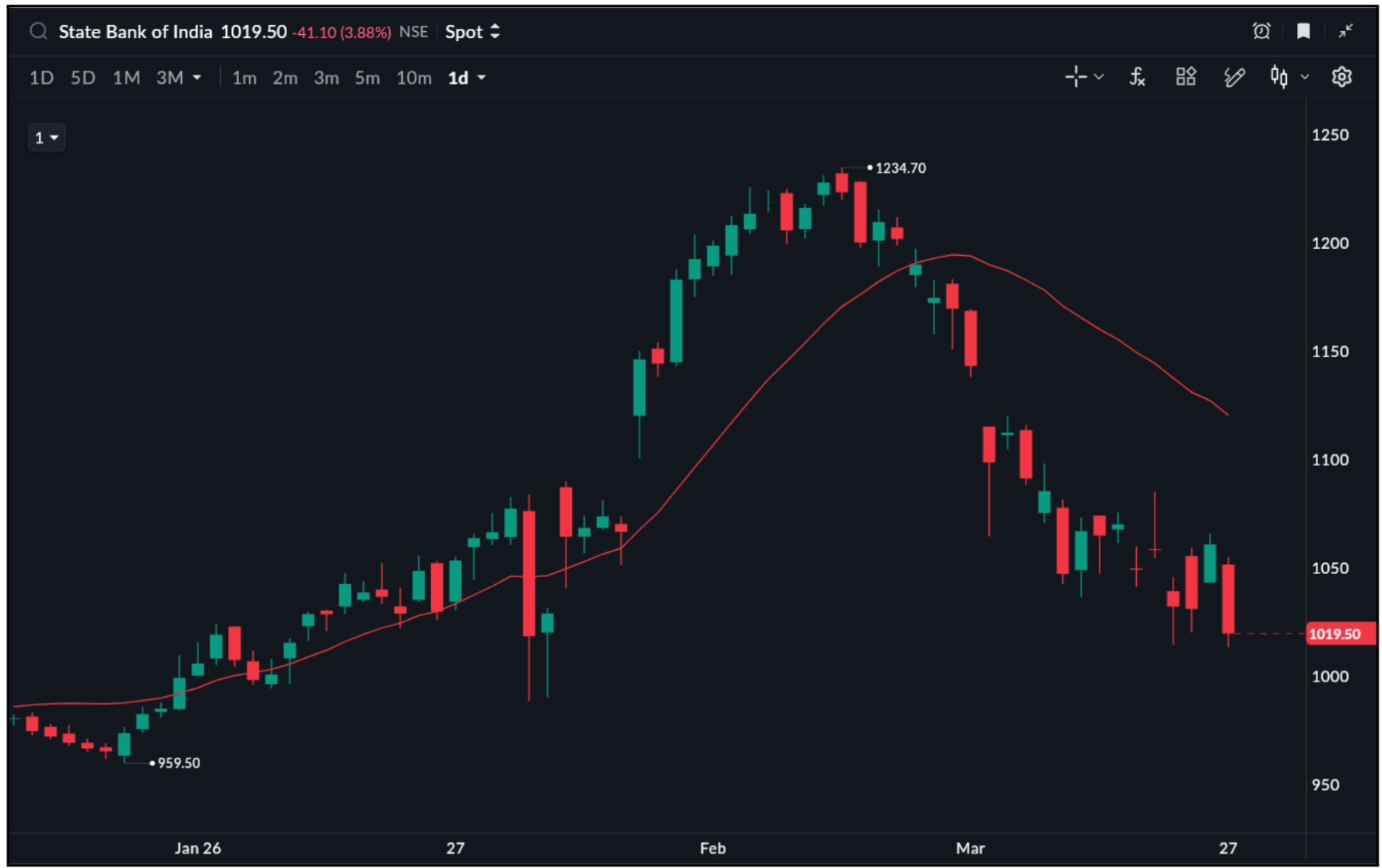

PSU bank stocks have had a rough few weeks — and Friday (27 March 2026) made it worse. The Nifty PSU Bank index closed down 3.86% at 8,249.45, making it the worst-performing sector of the day. Some individual stocks fell close to 5%.

No single thing caused this decline. It's a combination of problems that landed at roughly the same time.

What happened on March 27?

The PSU bank sell-off was part of a broader market crash. The Sensex fell 1,690 points to close at 73,583.22, and total investor wealth dropped by more than ₹8 lakh crore in a single session.

Not one PSU bank stock ended in the green. Bank of Baroda was the biggest loser at -4.55%, followed by Punjab National Bank (-4.49%), Canara Bank (-4.45%), UCO Bank (-4.10%), and Punjab & Sind Bank (-3.65%). SBI and Indian Bank fell around 2% and 4.10% respectively.

This wasn't a one-day event.

A brutal month for PSU banks

Over the past month, the Nifty PSU Bank index has fallen nearly 16.43% (as of 27 March 2026). Some stocks are down 20%.

| Bank | 1-Month Decline (%) |

|---|---|

| State Bank of India | 15.41% |

| Bank of Baroda | 19.34% |

| Canara Bank | 17.44% |

| Punjab National Bank | 18.92% |

| Indian Bank | 11.46% |

| Bank of India | 17.85% |

| Union Bank of India | 12.70% |

| Bank of Maharashtra | 14.87% |

| Indian Overseas Bank | 11.90% |

| Central Bank of India | 17.56% |

| UCO Bank | 20.40% |

| Punjab & Sind Bank | 16.27% |

Percentage decline as of 27 March 2026, 3:30 p.m.

Four main things are driving this.

Reason 1: The Iran-Israel-US conflict

The ongoing conflict involving Iran, Israel, and the US has pushed crude oil to around $107 per barrel. Every news cycle around the conflict — escalation, failed negotiations, ceasefire speculation — moves markets.

When oil rises, inflation fears follow. That pushes back expectations of rate cuts and hits rate-sensitive sectors hard. Banking is one of those sectors. PSU banks in particular hold large government bond portfolios that get repriced when the macro outlook shifts quickly.

Reason 2: Bond yields are rising fast

India's 10-year government bond yield hit 6.93% on March 27, the highest since July 2024. A week earlier it was at 6.76%.

This is worth understanding properly.

Banks aren't just deposit-and-loan businesses. Under SLR rules, they're required to hold a portion of deposits in government bonds. When bond yields rise, those bond prices fall — and banks have to record that as a loss (mark-to-market). This directly reduces treasury income, which contributes meaningfully to bank profits.

The government's FY27 gross borrowing target is ₹17.2 lakh crore. That kind of supply keeps the bond market under pressure, which means yields staying elevated isn't a short-term problem.

Reason 3: Fiscal concerns

The government recently cut excise duty on petrol and diesel, a welcome move for consumers, but it's raised questions about fiscal management. With crude already high, the subsidy bill grows too. Both together raise concerns about how much the government will end up borrowing beyond the budget estimate.

More borrowing means more bond supply, which feeds back into the yield problem.

Reason 4: Rupee at record low

The rupee fell to around 94.79 per dollar on March 27 — a record low.

Costlier dollars means costlier oil imports, which worsens inflation and complicates the RBI's rate decisions. Foreign investors pulling money out of Indian markets weakens the rupee further, which pushes more money out. For PSU banks, this extends the period of high yields and tightens the lending environment.

The bottom line

PSU banks are absorbing pressure from multiple directions — oil, bond yields, currency, and fiscal uncertainty — all at once. That's why the sector has taken a harder hit than most.

The underlying financials of these banks — credit growth, asset quality, capital adequacy — haven't fallen apart. This is a macro-driven correction. That distinction might not feel meaningful if you're watching these stocks fall 15-20%, but it does matter when thinking about what happens next.

Disclaimer: This article is for informational and educational purposes only. It does not constitute investment advice, a recommendation to buy or sell any securities, or an offer of any kind. The data and analysis presented reflect publicly available information as of 27–28 March 2026 and may not be current at the time of reading. Past performance of any stock or index is not indicative of future results. Investing in equities involves risk, including the possible loss of principal. Please consult a SEBI-registered investment advisor before making any financial decisions.