Why Indian Markets Fell Today? And Why It All Starts With a Hotel in Islamabad

The US-Iran peace talks in Islamabad collapsed, Trump announced a naval blockade, and oil surged back above $100. Here's exactly why Indian markets fell — and what the April 22 ceasefire deadline means.

Let's start with a room in a Pakistani hotel.

Over the weekend, something historic happened inside the Serena Hotel in Islamabad. For the first time since the Islamic Revolution of 1979, representatives of the United States and Iran sat across a table and actually talked. US Vice President JD Vance flew in, leading a delegation of nearly 300 officials. Iran sent its Foreign Minister Abbas Araghchi and Parliament Speaker Mohammad Bagher Ghalibaf. Pakistan — playing an unlikely mediator — had pulled off what most diplomats thought was impossible.

And then it all fell apart.

By Sunday morning, Vance was boarding Air Force Two, the negotiations having collapsed after 21 hours of talks. He put it plainly: Iran would not give the United States what it needed most — a firm, unambiguous commitment to abandon its nuclear weapons program. "The simple fact is that we need to see an affirmative commitment that they will not seek a nuclear weapon," Vance told reporters before departing.

Before most of Asia had even woken up, President Trump was on Truth Social announcing a US Navy blockade of all ships entering or leaving Iranian ports. By Sunday evening, crude oil had surged sharply back above $100 a barrel. And when Indian markets opened Monday morning, investors knew exactly what was coming.

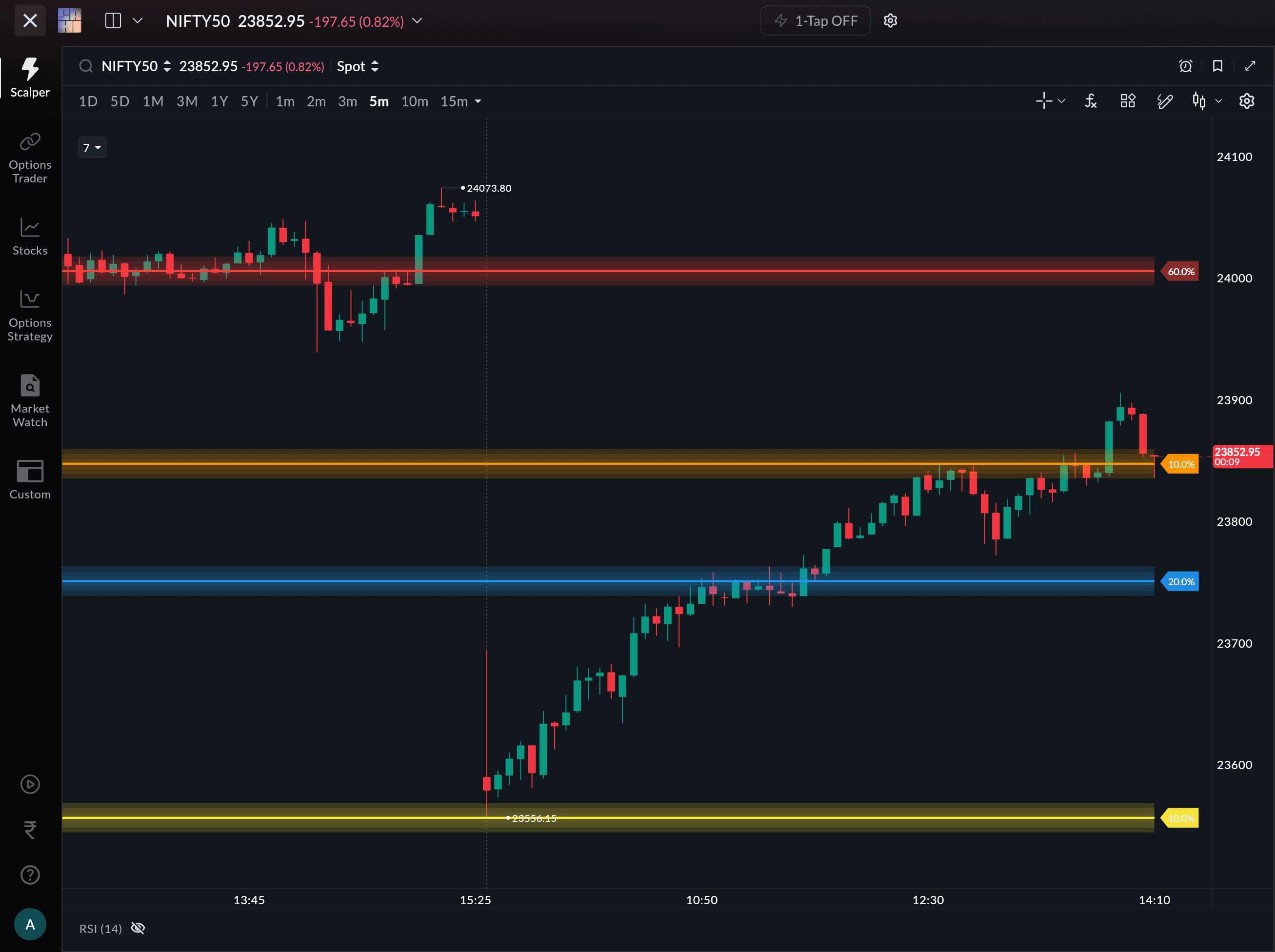

The Sensex fell over 1,400 points in early trade on April 13, sliding toward the 76,100–76,500 range. The Nifty dropped more than 400 points below 23,700. Market breadth was deeply negative — for every stock that rose, more than two fell.

So What Exactly Happened in Islamabad?

To understand today's market rout, you need to understand how we got here.

The US-Israel war on Iran began on February 28, 2026, with large-scale strikes that killed Iran's Supreme Leader. In retaliation, Iran's Islamic Revolutionary Guard Corps did something that rattled the entire global economy: it effectively shut the Strait of Hormuz.

That narrow strip of water — barely 34 kilometres wide at its tightest point — carries roughly 20% of the world's seaborne oil trade every single day. Saudi Arabia, Iraq, the UAE, Kuwait, and Iran all depend on it for their exports. When Iran closed it, tanker traffic collapsed. Brent crude, which was around $70 a barrel before the war, shot past $119 at its peak. The world had not seen an oil supply shock of this magnitude since the 1970s. We covered what that $119 spike meant for India's economy — and the reversal from the ceasefire, and now this renewed escalation, are following the same transmission channels.

A two-week ceasefire announced on April 7 offered brief relief. Oil prices fell nearly 15% in a single day. Hope returned that the strait would reopen and cooler heads would prevail.

Then Islamabad happened. The talks collapsed because the two sides were operating from entirely different realities. Washington wanted Iran to dismantle its nuclear enrichment program and commit to never acquiring a nuclear weapon. Tehran wanted guarantees that the war was truly over — that the bombing would not restart the moment it made concessions — and demanded continued control over the Strait of Hormuz, including the right to charge ships for passage. Iran's Parliament Speaker Ghalibaf said the US "ultimately failed to gain the trust of the Iranian delegation." The US called it Iran's refusal to accept a final, best offer. Vance said the US had been "quite accommodating" and that the US had made its "best, final offer."

Neither side thinks it lost the war. And that is the problem.

With no deal, Trump declared the naval blockade, oil prices surged back above $100-$105, and financial markets across Asia repriced the risk of a prolonged conflict overnight. The full timeline of the Iran-Israel war and its cost to Indian investors shows how each escalation has translated into market damage — and this is one of the sharpest reversals yet.

Why Does This Hit India So Hard?

Here is the uncomfortable truth about the Indian economy: we are almost entirely dependent on the rest of the world for our oil.

Even the markets reacted negatively with a gap down of over 1.5%, but recovered some of it, as the trading day progressed.

(Nifty50 image on SAHI, as of 2:15)

India's crude oil import dependence climbed to approximately 88.5–88.6% of total consumption in the first ten months of FY2025-26, an all-time high, according to data from the Petroleum Planning & Analysis Cell (PPAC). Every single day, India is consuming far more oil than it produces, and the gap keeps widening as domestic production from ageing fields continues to decline. Self-sufficiency in crude oil now stands at approximately 11–11.4% of consumption — meaning we produce barely one rupee of every nine we consume.

And who supplies the rest? The Middle East, primarily. Producers like Saudi Arabia, Iraq, and the UAE account for a large share of India's crude basket. Many of those shipments pass through or near the Strait of Hormuz. More than 50% of India's LNG imports also transit that strait.

So when the strait is blocked or threatened, India does not just face higher prices. It faces a structural vulnerability that feeds through the entire economy simultaneously.

The numbers are stark. Analysts estimate that a $10 increase in crude prices raises India's annual import bill by approximately ₹1 lakh crore to ₹1.1 lakh crore ($13–14 billion), widening the current account deficit by roughly 0.3% of GDP. Every 10% crude price shock can add approximately 30 basis points to inflation. A sustained $100-per-barrel oil price would significantly slow global economic growth — Wood Mackenzie has estimated it could drag global growth down toward 1.7%, from a pre-war forecast of around 2.5%.

India's crude basket price had already climbed sharply since the war began. With oil back above $100 and a US blockade potentially further tightening supply, the market is now pricing in a scenario where elevated oil prices are not a temporary inconvenience but a long-term reality.

The Bigger Picture: A Market Caught Between Two Uncertainties

There is a second layer to today's selloff that goes beyond oil. Markets hate uncertainty. And right now, there are two massive uncertainties sitting on top of each other.

The first is geopolitical. The ceasefire between the US and Iran expires on April 22. No new talks have been scheduled. Trump is reportedly considering limited military strikes to break the stalemate. Iran's IRGC has warned that any military vessels approaching the Strait of Hormuz will be dealt with "harshly and decisively." Analysts at the International Crisis Group describe the likeliest outcome as "not immediate war, but a volatile period of pressure, signalling, and last-minute attempts to prevent a wider conflagration." That is not a reassuring forecast for equity investors.

The second uncertainty is domestic. India's economy has been performing well, with strong consumption and manufacturing momentum. But if crude stays above $100 for an extended period, that strength faces a serious test. The Reserve Bank of India, which has been navigating a careful path on rates and liquidity, will have to contend with imported inflation at a time when it would prefer room to ease. The rupee, already under pressure, will face additional headwinds as the import bill widens and dollar outflows accelerate.

Goldman Sachs has warned that Brent crude could average above $100 a barrel for all of 2026 if the Strait of Hormuz remains largely blocked. An energy researcher at Columbia University was more direct, saying it could be a long time before prices come down even after the war ends, because damaged oil infrastructure will take months to repair and normal shipping routes will take time to reopen.

What Sectors Are Feeling It?

The impact is not uniform. Rising crude hits different parts of the market in different ways — and understanding that split matters for how you read today's moves. We broke down exactly which Indian stocks win and lose from crude price swings, the upstream vs downstream split is playing out again today, but now in reverse from the ceasefire rally.

OMC stocks — BPCL, HPCL, IOCL — are under pressure as rising crude squeezes their refining margins, especially when retail fuel prices remain government-controlled. Airlines like IndiGo face a direct hit as aviation turbine fuel costs rise. Paint, tyre, chemical, and plastics companies face higher feedstock costs. On the other side, upstream producers like ONGC and Oil India see their realised prices rise, which is positive for their earnings.

Beyond the direct energy plays, broader market sentiment is dragging financials, consumption, and rate-sensitive sectors lower — because elevated crude raises inflation expectations, limits RBI rate cuts, and weakens the rupee, all of which feed through to corporate earnings estimates over the next two to four quarters.

What Should You Watch Next?

The ceasefire technically holds until April 22. That date is the next major marker. Pakistan's foreign minister has said his country will try to facilitate a new round of dialogue in the coming days, but neither Washington nor Tehran has confirmed any plans to return to the table.

The US blockade of Iranian ports began on Monday morning. Whether that blockade holds, escalates, or is quietly softened as a negotiating tactic will determine whether oil prices stabilise or surge further. Some analysts view the blockade as a pressure tactic designed to force Iran back to the table rather than a permanent measure. If that reading is correct, a de-escalation could bring prices down quickly — just as the ceasefire announcement did ten days ago, pulling Brent down nearly 15% in a single session.

For Indian markets, the path forward is straightforward in theory and complicated in practice. If talks resume and the Hormuz situation eases, the selloff will reverse. If the conflict deepens and oil stays elevated, corporate earnings will be revised downward, the rupee will weaken further, and the RBI's policy options will narrow.

The world is waiting to see whether Islamabad was a temporary setback or the beginning of something worse. Indian equity investors, watching the Sensex and Nifty give back last week's gains in a single morning session, are watching the same thing — very carefully.

Disclaimer: This article is for informational and educational purposes only and does not constitute investment advice or a recommendation to buy or sell any securities. Market data reflects intraday levels on April 13, 2026, and is subject to change. Geopolitical situations are rapidly evolving — please verify the latest developments before making any decisions. Please consult a SEBI-registered financial advisor before making any investment decisions. SAHI is not responsible for any investment decisions made based on this content.