Crude Oil Price Crash: Why Some Indian Oil Stocks Went Up While Others Fell

The same crude oil crash sent OMC and aviation stocks up 6–10% and upstream producers down 4% on the same day. Here's why — and what investors should watch next

Global crude oil prices just took one of their sharpest single-day falls in decades, and Indian markets responded immediately. After the US and Iran agreed to a two-week ceasefire brokered by Pakistan, Brent crude plunged nearly 15% to around $92–95 per barrel, snapping a run that had seen oil trade above $110 for weeks following the near-closure of the Strait of Hormuz. The Nifty jumped over 3.64% by 12:10 p.m. on April 8, 2026, a direct read of how much relief this news brought to an import-heavy economy.

But here is what most market commentary missed: the same event that sent one set of oil stocks sharply higher sent another set sharply lower. To understand why, you need to understand that "oil sector" is not one thing. It is at least three very different businesses, and crude prices affect each of them in opposite ways.

What Actually Happened: The Strait of Hormuz Context

Since late February 2026, when US and Israeli airstrikes on Iran triggered retaliatory attacks on commercial shipping, the Strait of Hormuz had been effectively closed to normal traffic. The Strait is the world's single most important oil chokepoint, roughly 20% of global oil supply passes through it. Its disruption caused the largest oil supply shock on record, pushing Brent crude from around $70 a barrel in late February to over $110 in early April.

The ceasefire announcement changed this situation within hours. Trump said the two-week pause was conditional on Iran allowing safe passage through the Strait. Iran confirmed it would permit transit. Markets immediately priced out the geopolitical risk premium that had been built into oil prices over six weeks — and the result was a historic single-day fall. We covered what that price surge meant for India when oil crossed $119 — and the reversal is equally significant in the other direction.

Why Some Oil Stocks Went Up

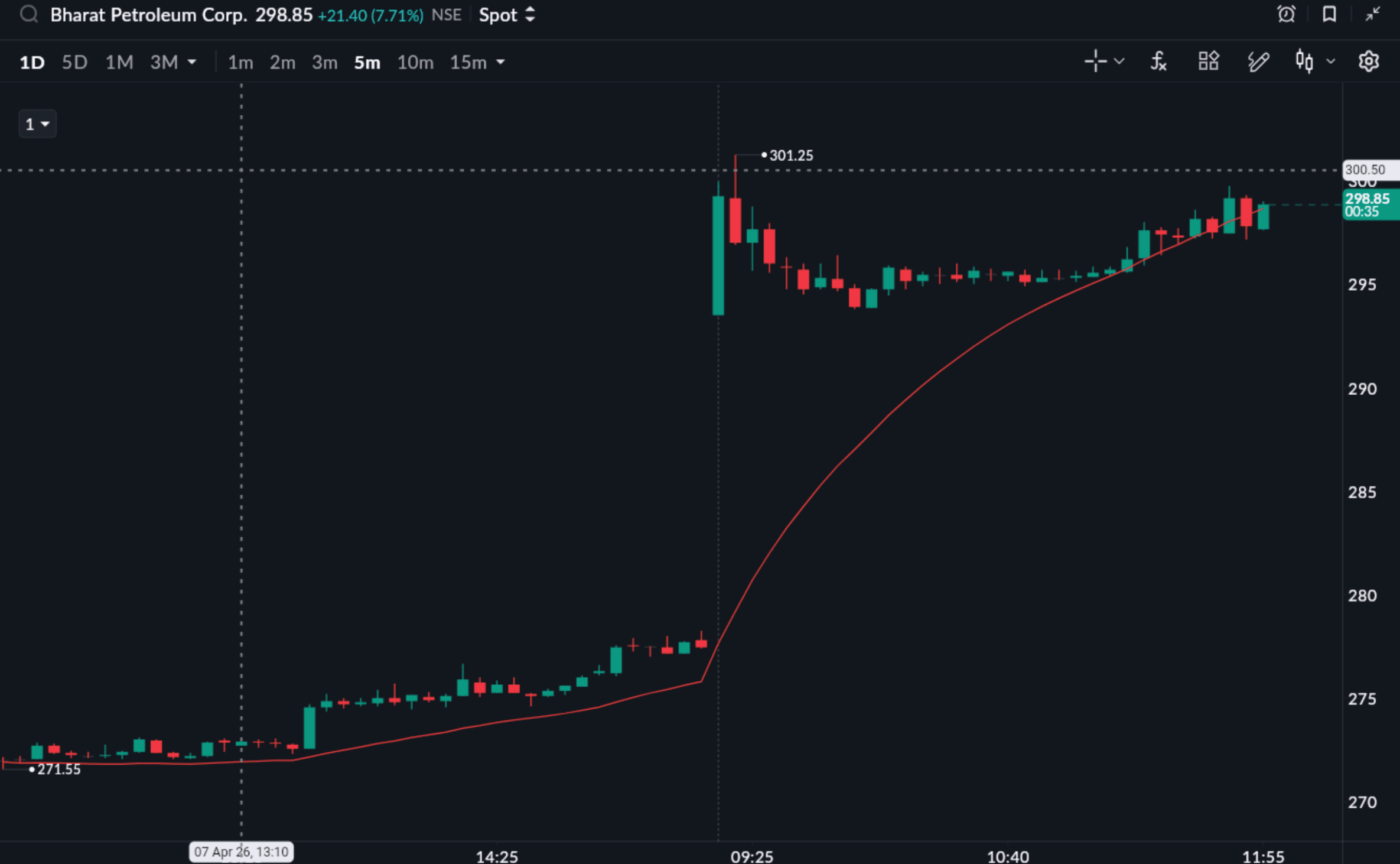

1. Oil Marketing Companies (OMCs) Got a Big Boost

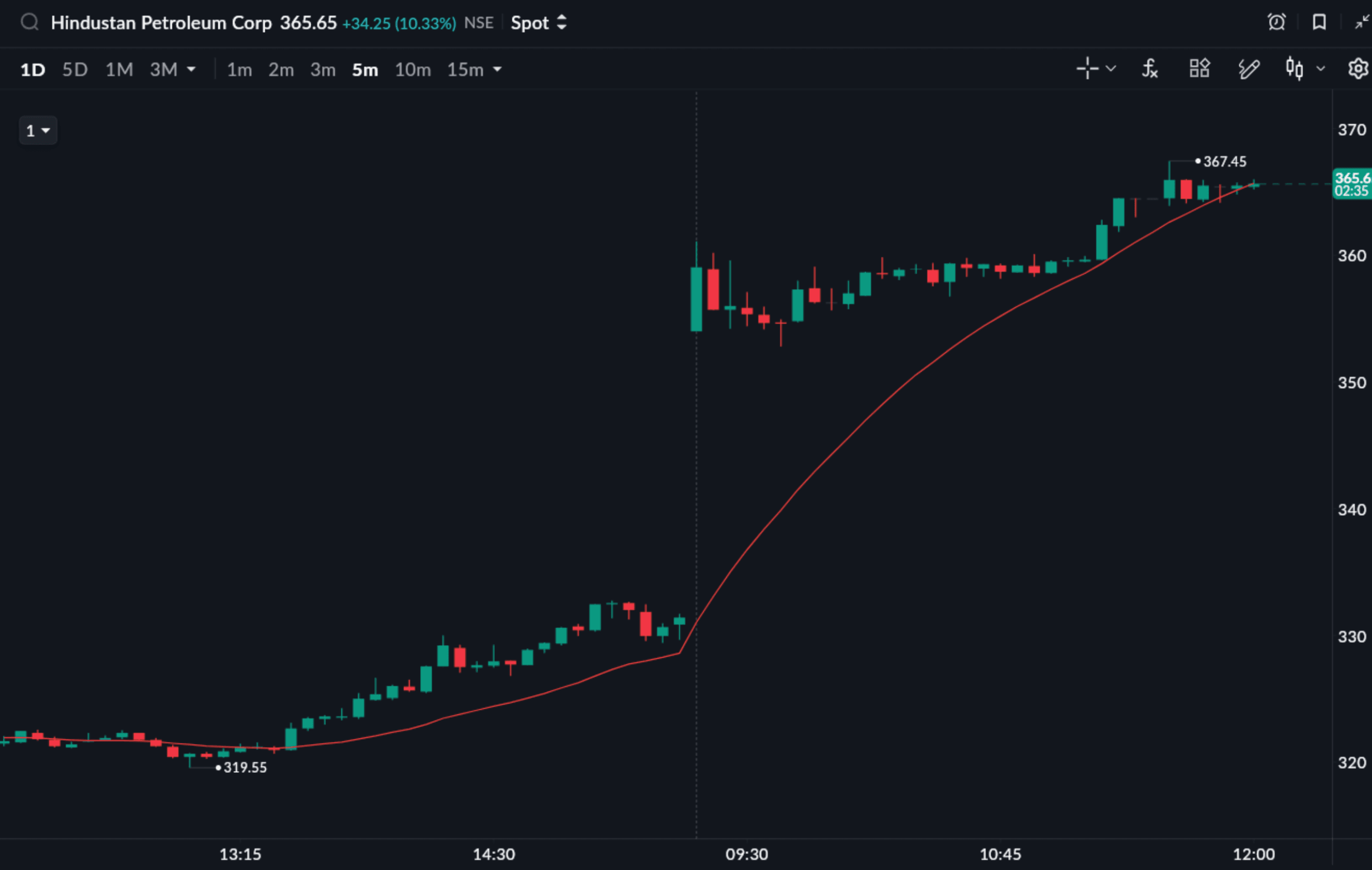

Companies like BPCL, HPCL, and IOCL were among the biggest winners, with stocks rising 6–9% on the day. HPCL jumped as much as 10.26% by 11:48 a.m.

(As of 11:59 a.m)

(As of 12:00 p.m)

These companies do not produce oil, they buy crude, refine it into petrol, diesel, LPG, and other products, and sell those to consumers. Their economics are built around one key variable: the refining margin, which is the gap between what they pay for crude and what they earn from selling refined products.

When crude becomes cheaper:

- Their input cost drops immediately

- If retail fuel prices hold steady, their margins widen

- Profitability improves, sometimes sharply

Think of it this way: if your raw material just got 15% cheaper overnight but you're still selling at the same price, you make more money per unit. That is precisely the dynamic playing out for OMCs here. The catch — which we'll return to — is that the government controls retail fuel prices in India, so the full margin benefit doesn't always flow through to earnings immediately.

2. Reliance and the Broader Refining Space

Reliance Industries also moved higher as the downstream refining and petrochemicals space rallied broadly. Reliance operates one of the world's largest and most complex refining setups at Jamnagar, and crude oil is a primary input cost across both its energy and chemicals businesses. Lower crude prices reduce input costs, which supports margins, particularly in petrochemicals, where pricing is competitive and margin defence matters.

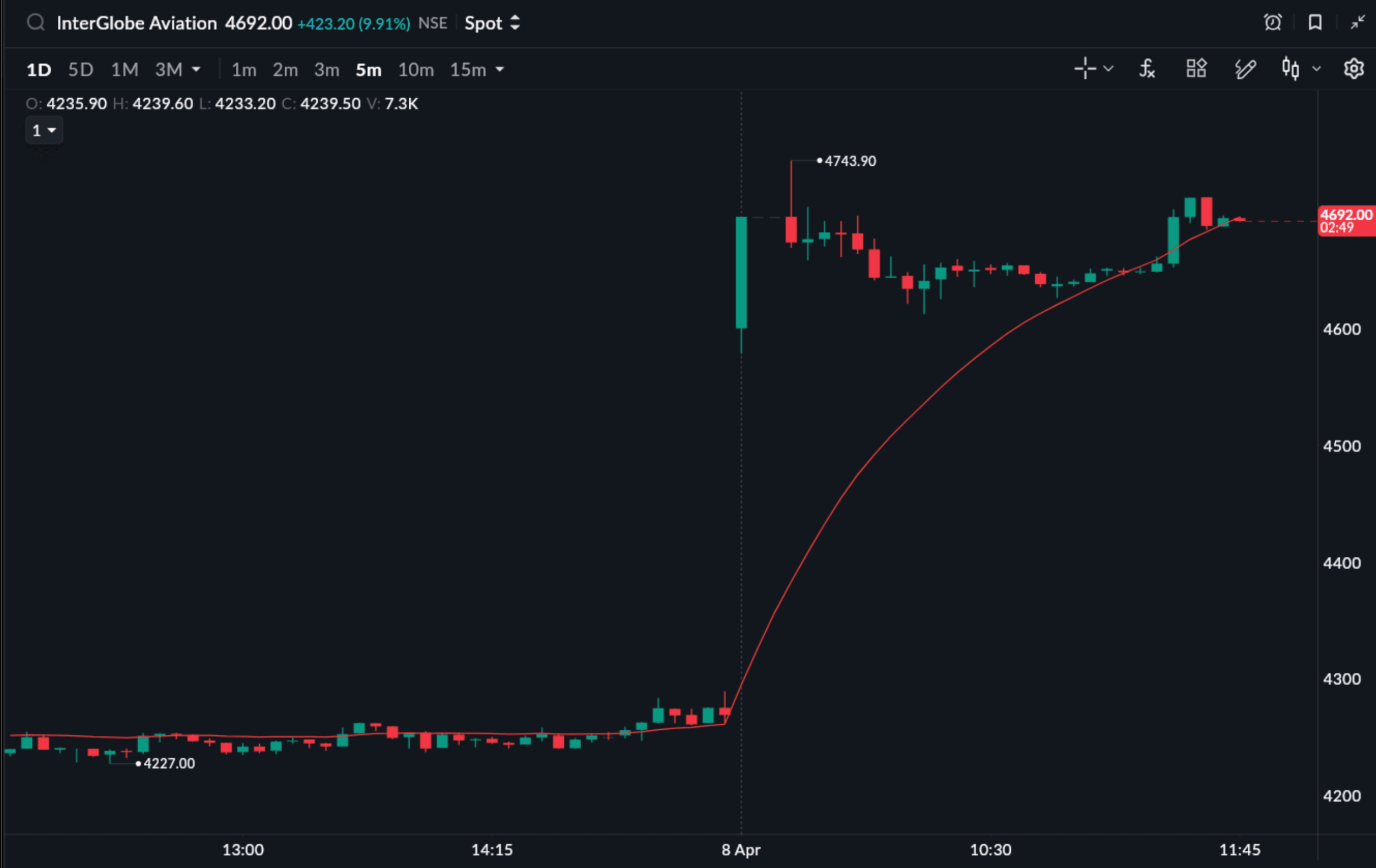

3. Aviation Stocks: The Biggest Surprise Winner

IndiGo's stock jumped nearly 10% by 11:47 a.m. on April 8, and this had nothing to do with producing or refining oil.

(As of 12:05 pm)

Aviation turbine fuel (ATF) is derived from crude oil, and it typically accounts for 35–45% of an airline's total operating costs. That makes airlines among the most oil-sensitive businesses in the entire market. When crude falls sharply:

- Fuel costs drop significantly

- Operating margins improve

- The airline becomes structurally more profitable at the same load factors and fares

Aviation stocks are, in many ways, an indirect bet on the oil price. When crude is high, airlines bleed. When crude falls, they breathe. A 15% drop in crude is an enormous tailwind for any airline's cost base. The inverse was true during the Gulf crisis escalation — airlines were among the most exposed names in the portfolio.

Why Some Oil Stocks Fell

Here is where the logic flips entirely.

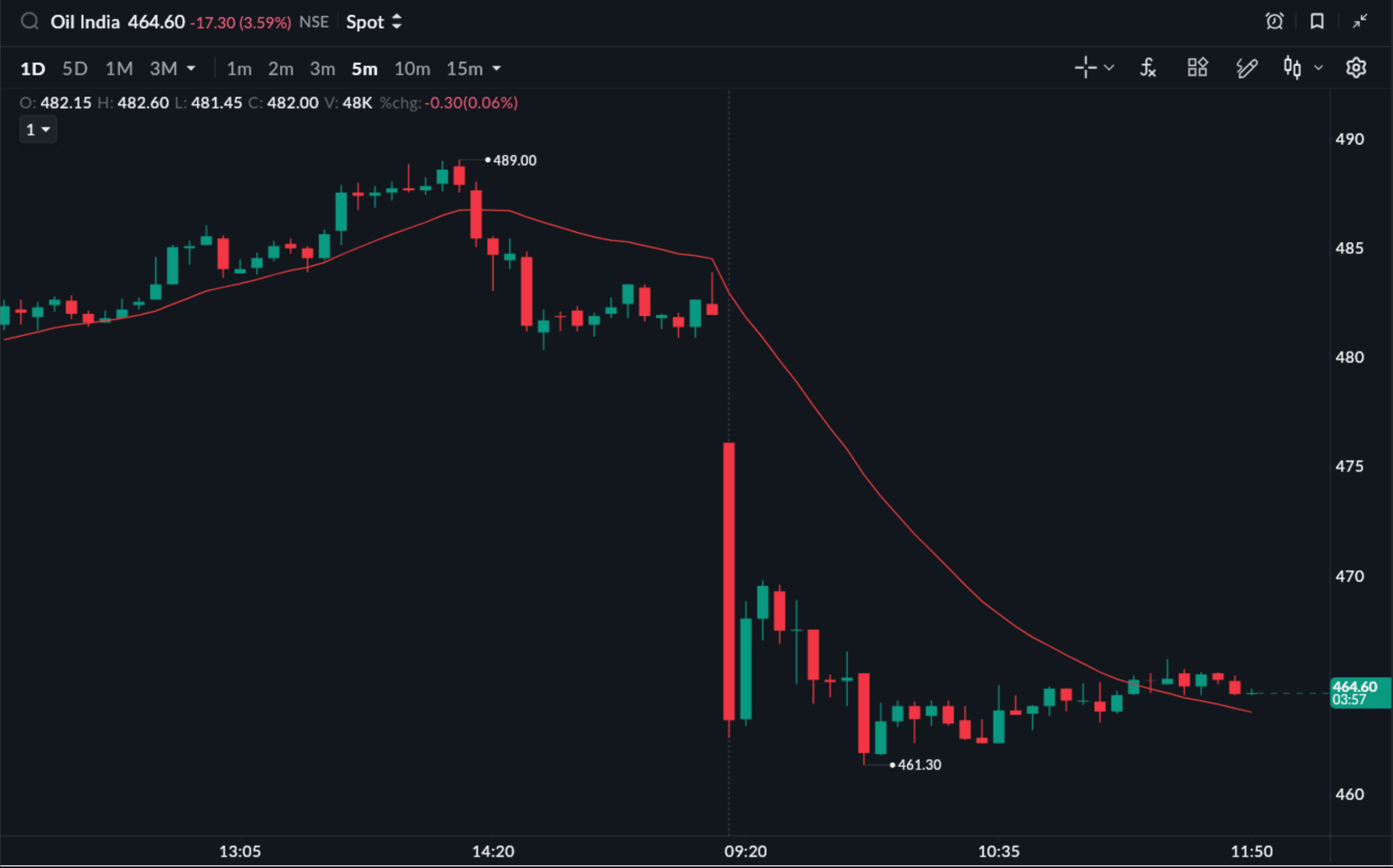

ONGC and Oil India — India's two largest upstream oil producers — both fell around 4% on the same day that OMCs and airlines surged. This is not a contradiction. It is a direct reflection of how different their business model is.

(As of 12:05 pm)

Upstream companies are in the business of finding oil underground, drilling for it, and selling it. Their revenue is almost entirely a function of one number: the price of crude oil in global markets. When that price goes up, they earn more per barrel. When it falls, they earn less.

There is no refining margin to fall back on. No opportunity to benefit from the gap between input cost and output price. The crude price IS the output price. So:

- Oil price up → upstream revenue up → stock up

- Oil price down → upstream revenue down → stock down

A 15% fall in Brent crude is, arithmetically, a 15% hit to the revenue per barrel that ONGC and Oil India realise on their production. That is a significant earnings headwind, and the market priced it in immediately. Understanding how oil prices transmit through different sectors of the Indian economy is essential context here — the same price movement affects companies in structurally opposite ways depending on where they sit in the value chain.

The Core Lesson: Upstream vs Downstream

This episode is a clean illustration of one of the most important distinctions in the oil sector:

Upstream companies (ONGC, Oil India) explore and produce crude oil. They are long crude, they benefit when prices rise and suffer when prices fall.

Downstream companies (BPCL, HPCL, IOCL, Reliance) refine crude into products and sell them. They are effectively short crude as an input cost — they benefit when prices fall (lower input cost) and suffer when prices rise (margin compression).

Adjacent sectors like aviation, paints, tyres, chemicals, and plastics are also indirect beneficiaries of falling crude, since their input costs — ATF, petrochemicals, polymers — all derive from oil.

The same news event, the same 15% oil price fall, created winners and losers simultaneously — and the direction depended entirely on which part of the oil value chain each company sits in. The macro transmission of crude prices through India's economy runs through all of these channels at once.

What Happens Next?

Everything now depends on whether the ceasefire holds and whether the Strait of Hormuz actually reopens to normal commercial traffic.

If it holds and oil flows normalise:

- Crude prices could fall further toward pre-war levels near $70

- OMCs, airlines, and other downstream consumers would see sustained margin improvement

- India's current account deficit would narrow, reducing rupee pressure

If tensions re-escalate or the ceasefire breaks down:

- The risk premium returns to oil prices quickly

- The entire trend reverses, potentially sharply

- Upstream companies recover and downstream companies come under pressure again

It is worth noting that Brent at $92–95, even after the fall, is still well above the ~$70 level before the war began. Full normalisation will take time — if it happens at all.

One Important Catch for OMCs

Even though falling crude sounds straightforwardly good for BPCL, HPCL, and IOCL, the full benefit does not always flow through to earnings immediately. A few reasons for this:

- Government price control: Retail petrol and diesel prices in India are not freely market-linked. The government can hold prices steady or adjust them on its own timeline, which means OMC margins may not widen as much as the crude fall implies.

- LPG under-recoveries: OMCs often sell LPG below cost. When crude falls, this under-recovery gap narrows — which is a positive — but it does not vanish entirely.

- Inventory effects: Refiners hold crude in inventory. If they bought expensive crude at $110+ and are now refining it in a $95 environment, the immediate margin may not reflect today's spot price.

Stock prices move instantly on news. Earnings take one or two quarters to reflect the actual change in the cost environment. That lag is worth keeping in mind before drawing strong conclusions from a single day's move.

What This Really Means for the Market

The April 8 session is a textbook example of how a single geopolitical event ripples through an interconnected market in different directions. One ceasefire announcement led to a historic fall in crude oil, a 3.64% Nifty rally, sector-wide winners in downstream energy and aviation, and simultaneous losers in upstream production — all within hours.

The takeaway for investors is straightforward: never treat a sector as monolithic. "Oil stocks" are not one trade. Knowing whether a company produces crude or consumes it as a raw material is the difference between being on the right and wrong side of a 10% move in a single session.

Disclaimer: This article is for informational and educational purposes only and does not constitute investment advice or a recommendation to buy or sell any securities. Stock price movements cited reflect intraday levels as of April 8, 2026, and are subject to change. Please consult a SEBI-registered financial advisor before making any investment decisions. Sahi is not responsible for any investment decisions made based on this content.