Waaree Renewable Q4 FY26: Revenue Doubles, Stock Jumps 13%. What the Numbers Say?

Waaree Renewable Technologies doubled revenue in Q4 FY26, with profits up 66% and a 2.83 GWp order book. Despite margin compression, the stock surged 13.5%. Here's the full picture.

Waaree Renewable Technologies Q4 FY26 Results: Waaree Renewable Technologies (WRTL) reported Q4 FY26 revenue of ₹1,102.4 crore — up 131% year-on-year — and net profit of ₹155.72 crore, up 66% YoY. For the full year FY26, revenue doubled to ₹3,331.42 crore (+108.5%) and PAT rose 109% to ₹478.65 crore. EBITDA margin for Q4 came in at 18.76% — below last year's 26.51% but above management's guided sustainable band of 14–16%. The unexecuted order book stands at 2.83 GWp, providing 12–15 months of revenue visibility. Shares surged 13.5% intraday on April 17, 2026. The board also approved the acquisition of a 55% stake in Associated Power Structures for ₹1,225 crore, expanding into power transmission infrastructure.

There is a saying in markets: the best earnings reports are not the ones with the biggest numbers. They are the ones where a company does exactly what it promised, and then some.

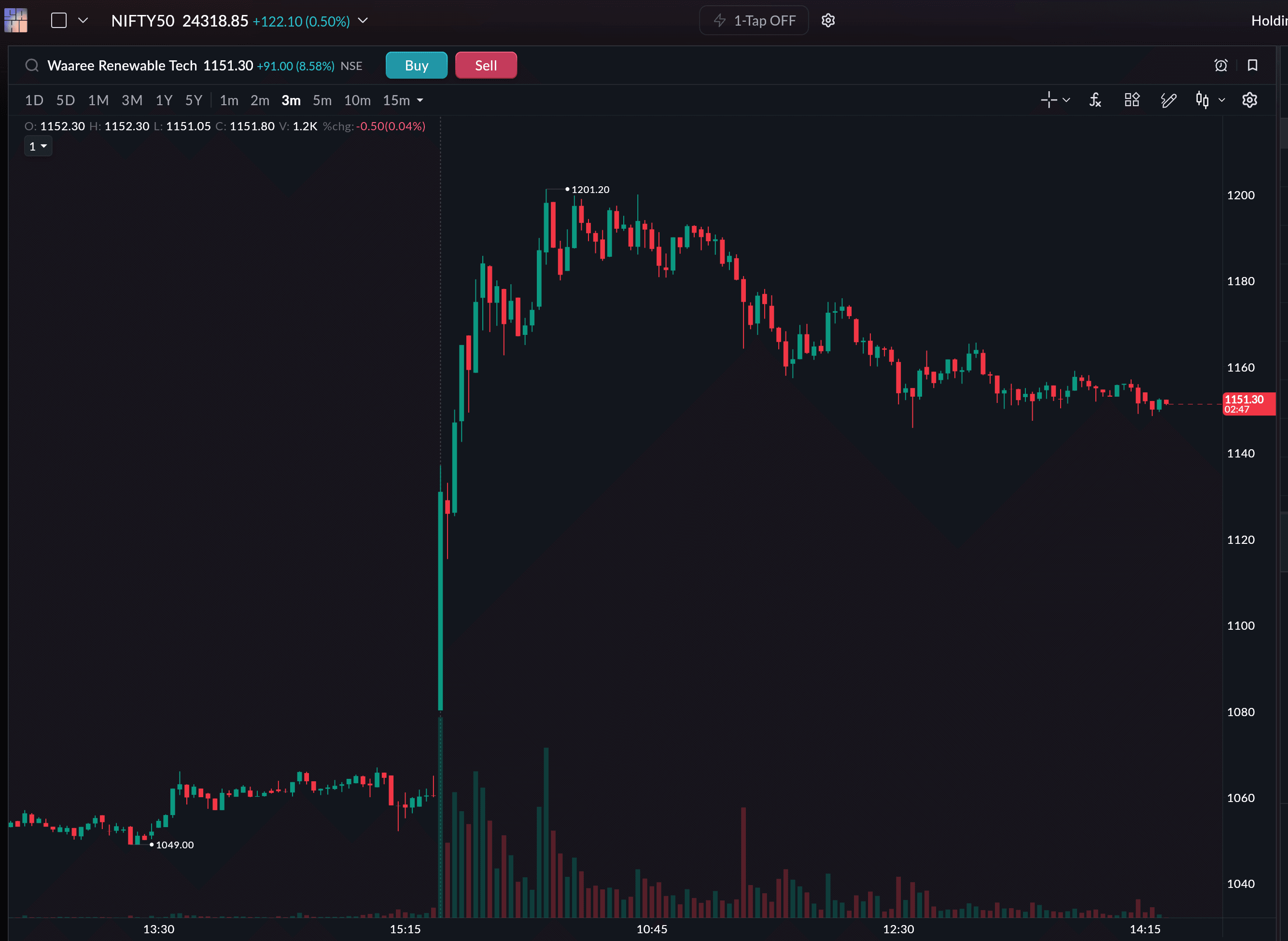

Waaree Renewable Technologies just had one of those mornings, which was also reflected in its stock price. (Stock price as of 2:20, 17th April)

(Stock price as of 2:20, 17th April)

On April 17, 2026, shares of the solar EPC company surged as much as 13.5% intraday after it dropped its Q4 FY26 results the previous evening. Revenue more than doubled. Profits jumped 66%. The order book is full enough to keep execution running for the next 12 to 15 months. And yet, buried inside the same report was a margin squeeze that, in any other quarter, might have spooked investors badly. They chose to look past it. Here is why that was probably the right call.

The Numbers

| Metric | Q4 FY26 | Q4 FY25 | YoY Change |

|---|---|---|---|

| Revenue from Operations | ₹1,102.40 crore | ₹476.58 crore | +131.3% |

| EBITDA | ₹206.82 crore | ₹126.33 crore | +63.7% |

| EBITDA Margin | 18.76% | 26.51% | −7.75 pp |

| Net Profit (PAT) | ₹155.72 crore | ₹93.76 crore | +66.1% |

Source: Waaree Renewable Technologies Q4 FY26 audited results, BSE/NSE filing, April 16, 2026

| Metric | FY26 | FY25 | YoY Change |

|---|---|---|---|

| Revenue from Operations | ₹3,331.42 crore | ₹1,597.75 crore | +108.5% |

| EBITDA | ₹641.10 crore | ₹310.90 crore | +106.2% |

| EBITDA Margin | 19.24% | 19.47% | Broadly stable |

| Net Profit (PAT) | ₹478.65 crore | ₹228.92 crore | +109.1% |

| Return on Equity (ROE) | 68.93% | — | — |

| Return on Capital Employed (ROCE) | 62.54% | — | — |

| Debt/EBITDA | 0.07x | — | Virtually debt-free |

Source: Waaree Renewable Technologies FY26 annual results, BSE/NSE filing, April 16, 2026

What Does Waaree Renewable Actually Do?

Waaree Renewable Technologies, which is often referred to as WRTL, is the EPC (Engineering, Procurement, and Construction) arm of the Waaree Group, India's largest solar module manufacturer with a capacity of approximately 26 GWp. WRTL does not just supply solar panels. It takes on full projects, designs the plant, sources the equipment, builds it, commissions it, and hands it over to the client. Think of it as the contractor that builds the solar farm, not just the factory that makes the bricks. The parent handles modules; WRTL handles construction and execution. The results suggest this division of labour is working extremely well.

Three Reasons the Stock Surged

India's solar boom is real, and WRTL is at the center of it. India added over 44 GW of solar capacity in FY26 alone — nearly double the approximately 24 GW added in FY25. As of March 2026, India's total installed renewable capacity had crossed 274 GW, with solar contributing over 150 GW. When the pie grows that fast, companies with the execution capability to win and deliver large projects grow with it. WRTL has now commissioned 5.06 GWp of projects in total and has 2,832 MWp currently under active execution.

The order book is locked-in future revenue. EPC businesses are particularly interesting because their order books represent future revenue already contracted. Once a company wins a contract to build a 420 MW solar farm, that money is coming — barring cancellations or delays. WRTL's unexecuted order book of 2.83 GWp provides 12–15 months of clear execution visibility. The bidding pipeline stands at over 36 GWp. Even winning a modest fraction of that would keep the execution engine running at full capacity well into FY27 and FY28.

High returns, no meaningful debt. Rapid growth usually comes with a balance sheet catch. WRTL has largely avoided this trap. The company remains virtually debt-free, with a Debt/EBITDA ratio of just 0.07x. ROE for FY26 stood at 68.93% and ROCE at 62.54%. High returns, no meaningful debt, doubling revenue — that combination is what makes institutional investors move fast. A similar pattern of institutional accumulation is playing out in India's wind sector too.

Order Book and Execution Pipeline

| Metric | Status (as of Q4 FY26) |

|---|---|

| Total projects commissioned to date | 5.06 GWp |

| Projects currently under execution | 2,832 MWp (2.83 GWp) |

| Expected execution timeline | 12–15 months |

| Bidding pipeline | Over 36 GWp |

| Notable Q4 FY26 new orders won | 420 MWp ground-mounted, 35 MWp, 14 MWp ground-mounted |

Source: Waaree Renewable Technologies Q4 FY26 results commentary; CFO statement, April 16, 2026

The Margin Story — What Investors Chose to Overlook

Not everything in these results was gleaming. EBITDA margin for Q4 FY26 declined to 18.76%, down from 26.51% in Q4 FY25. That is a meaningful compression driven by competition, pricing pressures, and a shift in project mix toward larger, lower-margin utility contracts.

For many companies, a margin decline of this magnitude would trigger a sell-off. The stock rose instead, for a specific reason: management had previously guided for sustainable EBITDA margins of 14–16%. When the actual Q4 margin came in at 18.76%, above that guided band despite the year-on-year decline, it was read as a positive. The company has been transparent that as it scales rapidly and operates in a more competitive bidding environment, margins will face pressure. What investors needed to see was whether margins were settling at a sustainable level or deteriorating uncontrollably. The answer, this quarter, was the former.

There is also a scale argument at work. Even at compressed margins, a company doing ₹1,102 crore of quarterly revenue generates far more absolute profit than the same company doing ₹476 crore at fatter margins. Volume is doing the heavy lifting.

The Associated Power Structures Acquisition

One strategic move in this results cycle that deserves attention: WRTL's board approved the acquisition of a 55% stake in Associated Power Structures (ASPL) for ₹1,225 crore (a mix of primary and secondary transactions), subject to due diligence and customary closing conditions.

| Acquisition Detail | Value |

|---|---|

| Target company | Associated Power Structures (ASPL) |

| Stake being acquired | ~55% |

| Total consideration | ₹1,225 crore (primary + secondary) |

| ASPL's business | Power transmission and distribution infrastructure |

| ASPL established | 1996 |

| Post-acquisition status | ASPL becomes a subsidiary of WRTL |

Source: Waaree Renewable Technologies board resolution, January 26, 2026; NSE/BSE filing

As India's solar capacity grows, the transmission infrastructure to carry that electricity becomes equally critical. WRTL is positioning itself to capture that opportunity—building a platform that spans renewable generation EPC, energy efficiency, and supporting grid infrastructure. India's broader energy transition is creating demand across the entire clean energy stack, and WRTL is building exposure to multiple parts of it.

What to Watch

The stock has had a sharp run and valuations are not cheap by any measure. The key variable in FY27 is the margin trajectory — if competition intensifies further or project mix shifts unfavorably, margins could compress below the 14–16% guided band. Battery Energy Storage Systems (BESS) is also an area WRTL is developing. As India grapples with the intermittency of solar power, storage becomes the next frontier. Whether WRTL can execute effectively in this newer segment — beyond its established EPC strengths — will determine the next chapter of the growth story.

Disclaimer: This article is for informational purposes only and does not constitute financial advice. All financial figures are sourced from Waaree Renewable Technologies' audited Q4 FY26 results filed with NSE/BSE on April 16, 2026. Please consult a SEBI-registered advisor before making investment decisions.