SAIL Stock Jumps 15%: How the Steel PSU Delivered 65% Returns in 1 Year

From a Morgan Stanley Underweight at ₹105 to a 52-week high of ₹192, here is how SAIL went from sector laggard to one of the year's sharpest PSU reversals.

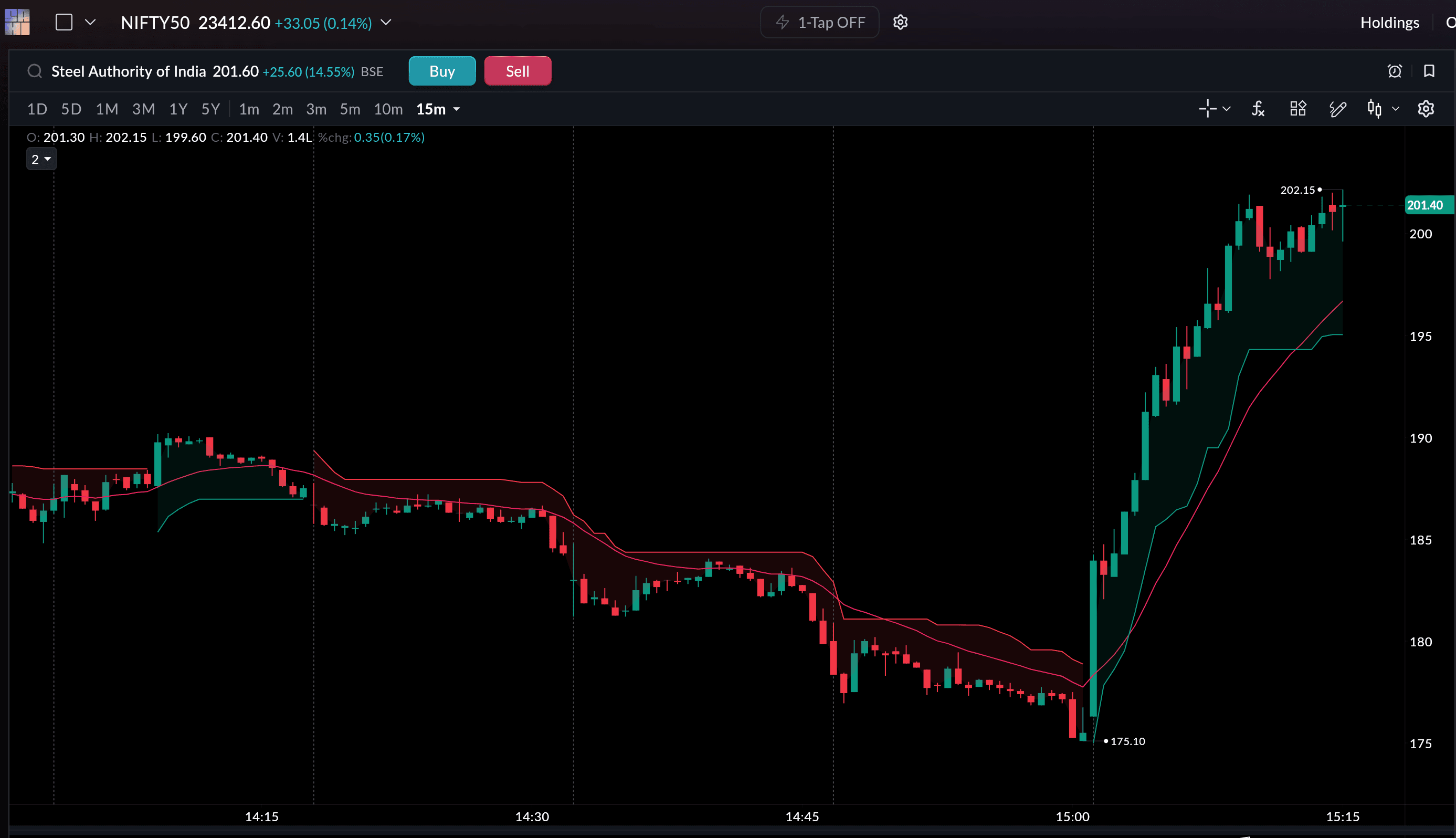

SAIL stock surged nearly 15% to a 52-week high of ₹192 on 13 May 2026, delivering 52–65% returns over one year. The rally follows a government 12% safeguard duty on steel imports, a 163.6% jump in Q3 FY26 net profit, and an F&O ban on NSE that is pushing traders into cash market buying. The board meets on 15 May to approve Q4 and full-year FY26 audited results.

There is a stock on Dalal Street today that has done something it has not managed in six years. Steel Authority of India Limited, better known as SAIL, has surged nearly 15% in a single session, touching a 52-week high of ₹192 and briefly crossing ₹201 on some platforms. For a public sector steel company that investors had written off as slow, bureaucratic, and perpetually at the mercy of commodity cycles, this is a remarkable moment.

So what exactly is going on?

To understand today, you need to go back about a year.

The problem that would not go away

India's steel industry spent much of FY2024-25 in a state of quiet anxiety. Cheap steel from China, South Korea, and Japan was flooding the Indian market at prices that domestic producers simply could not match. In FY25, India imported approximately 9.5 million metric tons of finished steel, the highest volume in nearly a decade. The country had become a net importer of finished steel for the second year running.

The consequences were brutal. Domestic steel prices crashed to around ₹47,000 per tonne, near a yearly low. Margins at Indian steelmakers collapsed. SAIL, with its five integrated plants and three special steel facilities largely concentrated in the eastern and central regions of India, was among the worst-affected. The company's return on equity hovered around a dismal 4.86% over the prior three years. Analysts from Morgan Stanley had slapped an Underweight rating on the stock with a target price of ₹105. Nuvama had downgraded it to a Hold and slashed its target sharply. The narrative around SAIL was essentially this: a lumbering public sector giant with high contingent liabilities of over ₹44,000 crore, modest sales growth of just 10.7% over five years, and very little to get excited about.

Then the government stepped in.

The tariff that changed the calculus

In April 2025, after an investigation by the Directorate General of Trade Remedies, the government imposed a provisional safeguard duty of 12% on select steel flat products, including hot-rolled coils, cold-rolled sheets, metallic-coated products, and color-coated steel. The measure was aimed squarely at the surge of imports from China, South Korea, and Japan, which had been accused of selling below cost and distorting the Indian market. The provisional duty was confirmed as a final measure later in the year, and it will stay in place, stepping down gradually, until April 2028.

The impact was immediate and significant. Domestic steel prices recovered by roughly ₹5,000 per tonne, rising back toward ₹52,000. ICRA estimated that the safeguard duty alone could halve India's steel imports in FY2025-26. Capacity utilisation at domestic steelmakers was expected to climb from 78% to around 83%. For SAIL, which had been running plants at suboptimal rates and watching margins erode, this was exactly the relief it needed.

The numbers started turning. In Q3 FY2025-26, SAIL's revenues grew 11.4% year on year. Net profit jumped a remarkable 163.6% over the same period a year earlier, though it dipped slightly quarter on quarter. For the full year FY2025-26, revenue reached ₹1,03,354 crore, with profit coming in at ₹1,885 crore. The board is scheduled to meet on May 15 to approve audited Q4 and full-year results, and the anticipation of a strong fourth quarter is adding fuel to the fire right now.

And then there is the F&O twist

Here is where today's 15% jump gets an extra layer of complexity.

SAIL is currently under an F&O ban on the NSE. This means that its open interest in futures and options contracts has crossed 95% of the market-wide position limit. As of this morning, SAIL's open interest sat at 106% of the MWPL, well above the threshold. The ban prevents traders from initiating any fresh derivative positions. They can only square off or reduce existing ones.

Now, this sounds like it should be bad for the stock. No new bets allowed. But here is the paradox. When a high-conviction rally is already underway, an F&O ban can actually amplify cash market buying. Traders who want exposure to the stock but cannot use futures or options must simply buy shares outright in the cash segment. That added demand, on top of an already bullish undertone, creates the kind of explosive move you are seeing today.

The stock touched a fresh 52-week high of ₹192.21 during the session, a level it has not visited in years. The 1-year return on SAIL now stands at roughly 52% to 65%, depending on where you measure from.

The bigger picture

It is worth stepping back and asking whether this rally reflects genuine value creation or simply the confluence of policy support and short-term trading dynamics.

The honest answer is probably both.

The structural tailwinds are real. India's steel consumption grew 8.1% year on year in April 2026. Infrastructure spending under the government's capital expenditure push continues to drive demand for long steel products, exactly the kind SAIL produces in bulk. The company has a long record of supplying steel for projects of national importance, from the Mumbai-Ahmedabad bullet train corridor to the Kalpakkam nuclear facility to expressways across the country. As these projects scale, order books hold up.

The safeguard duty, while not a permanent wall, buys time for domestic steelmakers to recalibrate, invest in efficiency, and compete on better terms. SAIL has been quietly working on cost reduction, decarbonisation, and energy efficiency. Foreign institutional investors have been steadily increasing their stakes, a vote of confidence that was notably absent a year ago. Mutual fund holdings stand at 8.69% of the company.

But the risks are not invisible either. The government holds a 65% promoter stake, which limits the free float and can make the stock more volatile on lower volumes. The company's contingent liabilities remain large. And while the safeguard duty shields domestic producers for now, it is designed to taper down over three years. Steel is ultimately a cyclical business, and the same global forces that hurt SAIL in FY25 could return.

What this tells us

SAIL's rally is a reminder that the worst-loved stocks in a sector can deliver the sharpest reversals when conditions change. A year ago, it was a cautionary tale about bloated PSUs and commodity cycles. Today it is a story about policy intervention, earnings recovery, and the peculiar mechanics of derivative market bans.

The steel sector is not out of the woods. Global overcapacity persists. Chinese exports remain a structural challenge even with tariffs in place. But for now, SAIL is having its moment. The market is repricing a company that had been left for dead and finding, to its surprise, that the patient is doing rather better than the diagnosis suggested.

Whether this is the beginning of a sustained re-rating or a sharp bounce in a volatile name is a question each investor must answer for themselves.

Disclaimer: This article is for informational purposes only and does not constitute investment advice. Please consult a registered financial advisor before making investment decisions.