Ola Electric Share Price: Fall, Recovery & What's Next

Ola Electric's stock fell over 85% from its post-IPO high. Here's what actually went wrong, what the 46100 LFP cell announcement means, and whether the recent recovery is real.

There is a particular kind of company that captures the imagination of an entire market. It launches with fanfare, dominates headlines, goes public at a valuation that makes serious analysts raise an eyebrow, and then spends the next 18 months teaching everyone a very expensive lesson in the difference between a story and a business.

Ola Electric is that company. And right now, it sits at one of those rare inflection points where the answer to "buy or sell" genuinely depends on which version of the future you believe in.

Let us start from the beginning.

The Rise: Too Fast, Too Confident

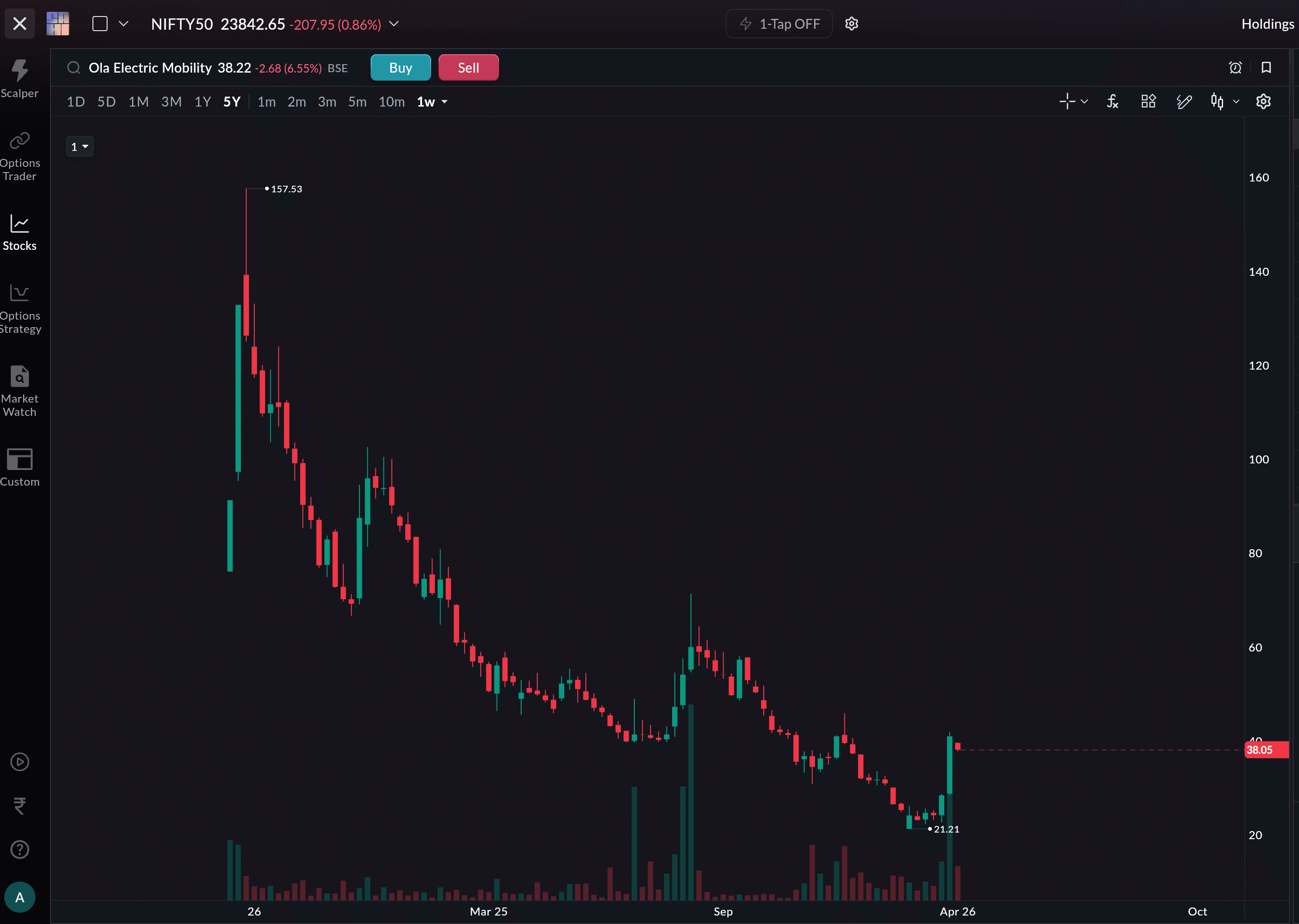

Ola Electric became India's bestselling electric two-wheeler brand within just nine months of its first scooter launch in late 2021. That is not a small feat — the company did not slowly grind its way to the top. When it went public in August 2024, the stock listed at its issue price of ₹76 per share. The market cap at listing implied a company worth tens of thousands of crores for a business that had never turned a rupee of profit.

The market was not being irrational. It was pricing in a vision: Ola as a vertically integrated EV-and-energy giant, making its own cells, its own motors, its own software. The "Tesla of India" framing was never far from the conversation.

But then reality began doing what it always does.

The Fall: When Customers Stop Being Forgiving

In 2025, Ola's market share dropped from approximately 35.5% to 16.1%, according to Vahan registration data. Registrations fell roughly 52% to approximately 1.97 lakh units, making it the only top player to shrink while TVS, Bajaj, and Ather grew. TVS Motor, in fact, overtook Ola to become the top-selling E2W brand in 2025 with 2.95 lakh units. While rivals posted record sales, Ola was dealing with rising consumer complaints about product quality and after-sales service.

(Stock price as of 13th April, after market hours)

The stock mirrored the decline. From its post-listing high of ₹157.40 in August 2024, the stock fell over 85% to hit an all-time low of ₹22.25 on March 16, 2026 — wiping out tens of thousands of crores in shareholder value. SoftBank, the company's biggest institutional backer, reduced its stake from over 17% at IPO to 13.53% as of January 2026. The bigger issue was simple: a tech-first story was undone by basic problems like faulty scooters and slow service. In India, for a ₹1.5 lakh purchase, trust is not a soft metric — it is a hard business requirement. That is what Ola lost.

Have the Fundamentals Changed?

This is the question that actually matters. Not whether the stock has bounced roughly 70% from its March lows — bouncing from a record low is a low bar. The real question is whether the underlying business is structurally different from what it was six months ago.

Honestly? The answer is: somewhat, but not decisively.

On the negative side, the financial picture remains grim. In Q3 FY26 (October–December 2025), Ola reported revenue of ₹470 crore — down 55% year-on-year and 32% quarter-on-quarter from ₹690 crore in Q2. Net losses were ₹487 crore, wider than ₹418 crore in Q2 FY26, though narrower than the ₹564 crore loss a year earlier. The company spent more losing than it earned selling. Operating profit has declined at an annual rate of approximately 38% over the last five years, and the interest coverage ratio remains deeply negative. The company's auditor flagged going concern risks due to negative cash flows from operations — ₹866 crore in the nine months to December 2025 — and continued operating losses.

On the positive side, three things are genuinely worth paying attention to.

First, sales appear to be recovering at the ground level. Registrations jumped from 3,973 units in February 2026 to 10,117 units in March — a meaningful sequential recovery, though analysts have raised questions about whether some of those March numbers reflect genuine demand or were boosted by a ₹49,999 aggressive pricing campaign that ended March 31. Over 80% of vehicles are now reportedly being serviced on the same day, a direct response to the after-sales crisis that triggered the collapse in the first place.

Second, the Gigafactory story is inching from ambition toward execution. The plant currently operates at 2.5 GWh capacity and is scaling to 6 GWh. Cell production doubled quarter-on-quarter in Q3 FY26 to 72,418 cells. Thousands of vehicles powered by Ola's 4680 Bharat Cells are already on Indian roads, collectively covering millions of kilometres of real-world use. The ramp-up in cell production has enabled a price cut of ₹60,000 on the Roadster X Plus 9.1 kWh model — a direct pass-through of manufacturing efficiency to the consumer.

Third, on April 7, 2026, Ola filed a regulatory disclosure announcing the readiness of its in-house developed lithium iron phosphate (LFP) cell in the new 46100 format — physically larger than the current NMC 4680 Bharat Cell, designed to deliver improvements in scale, cost efficiency, and versatility across both electric mobility and energy storage applications. What makes this notable is the speed. In its Q3 shareholder letter published in February 2026, Ola had said the 46100 LFP cell was 12 to 24 months away. The April 7 announcement, two months later, suggests the company moved significantly faster than it had guided the market to expect — though it is worth noting that no energy density figures, cycle life data, or third-party certifications have been published yet, and vehicle integration is said to begin "next quarter" rather than immediately.

If this cell goes into production at scale, it changes the cost structure meaningfully. LFP chemistry is cheaper to produce and does not require expensive cobalt or nickel, thermally more stable in India's climate, and opens the door to stationary energy storage. That would let Ola sell into the Battery Energy Storage Systems (BESS) market and diversify away from scooters entirely.

The Competition Problem Has Not Gone Away

Here is what the bulls tend to gloss over. Even if Ola's battery technology is real and the Gigafactory scales as promised, the competitive landscape of 2026 looks nothing like 2022.

Japanese OEMs including Yamaha, Honda, and Suzuki entered the electric two-wheeler space in 2025, raising consumer expectations around product refinement and reliability. Bajaj and TVS are no longer playing catch-up — they are winning. Ather Energy has surpassed Ola in both market capitalisation and quarterly revenue: Ather's Q3 FY26 revenue was ₹953.6 crore versus Ola's ₹470 crore. Our analysis of Ather Energy's IPO and business model covers exactly why Ather's approach — slower to scale, stronger brand equity — has paid off in the current environment.

The overall E2W market, meanwhile, has slowed from the explosive early-adopter growth phase. The first wave of EV enthusiasts has largely been served, and winning the next wave of mainstream buyers requires something Ola has struggled to deliver: consistent product quality and reliable after-sales. Brokerages including Citi and Emkay Global downgraded the stock to 'Sell' in early 2026, citing persistent headwinds and cutting target prices sharply. Delhi's new EV policy — which mandates electric-only two-wheeler registrations from 2028 — creates structural tailwinds for the entire sector, but the companies best positioned to capitalise on that are the ones with strong service infrastructure and brand trust today.

Ola is not fighting a weakening field. It is fighting a stronger one with a damaged reputation and a business model that has not yet demonstrated it can make money.

So Is It a Buy?

It depends on your time horizon and risk appetite.

The stock is well below its highs — trading around ₹38 on April 13, still roughly 50% below its IPO price of ₹76 — which may look attractive if you believe in Ola's long-term story. But for most investors, it may be better to wait for Q1 FY27 data (April–June 2026). The key question is whether the March sales recovery continues organically, or fades once the aggressive discount campaign ends.

If Ola executes on the 46100 LFP cell, the Gigafactory scale-up, and service improvements, the current market cap of approximately ₹18,000 crore could look cheap in hindsight. If not — if the March recovery fades, if the LFP cell takes longer than guided to reach vehicles at scale, or if competition continues to erode market share — the stock has further to fall.

Abhinav Tiwari, Research Analyst at Bonanza, puts it plainly: recent price cuts can help push volumes in the near term and recover some lost market share, but lower pricing alone is not enough if margins remain weak. Aggressive discounting may improve volume but delays profitability even further. India's auto retail sector has been growing strongly — the macro tailwind is real. But tailwinds help every player, not just the weakest one.

For now, the story is promising but unproven, and the next few quarters will matter more than any narrative.

Disclaimer: This article is for informational and educational purposes only and does not constitute investment advice or a recommendation to buy or sell any securities. Stock price and market cap data reflects levels as of April 13, 2026, and is subject to change. Financial figures cited are from company filings and publicly available sources. Please consult a SEBI-registered financial advisor before making any investment decisions. SAHI is not responsible for any investment decisions made based on this content.