HCL Tech's ₹4,488 Crore Quarter, and Why The Share Price Fell Around 9%?

HCL Tech posted a profit of ₹4,488 crore in Q4 FY26 — and yet the stock crashed 9%. Here's the real story behind the numbers.

Quick Answer

HCL Tech reported Q4 FY26 (January–March 2026) net profit of ₹4,488 crore (up 4.2% YoY) on revenue of ₹33,981 crore (up 12.3% YoY). Despite headline growth, HCLTech's share price crashed ~9% on April 22 due to EBIT margin compression to ~17.7% (adjusted) and conservative FY27 IT Services revenue growth guidance of just 1.5–4.5% in constant currency, well below analyst expectations.

Let's start with something that sounds contradictory.

HCL Technologies — India's third-largest IT company — just reported a profit of ₹4,488 crore for the January–March quarter of FY26. That's a 4.2% jump from the same quarter last year. Revenue crossed ₹33,981 crore, up 12.3% year-on-year. The company won deals worth $1,936 million in a single quarter. And to top it all, management declared an interim dividend of ₹24 per share, alongside ₹36 already paid through three quarterly installments during FY26, bringing the total dividend associated with the year to ₹60 per share.

By most definitions, that's a solid quarter.

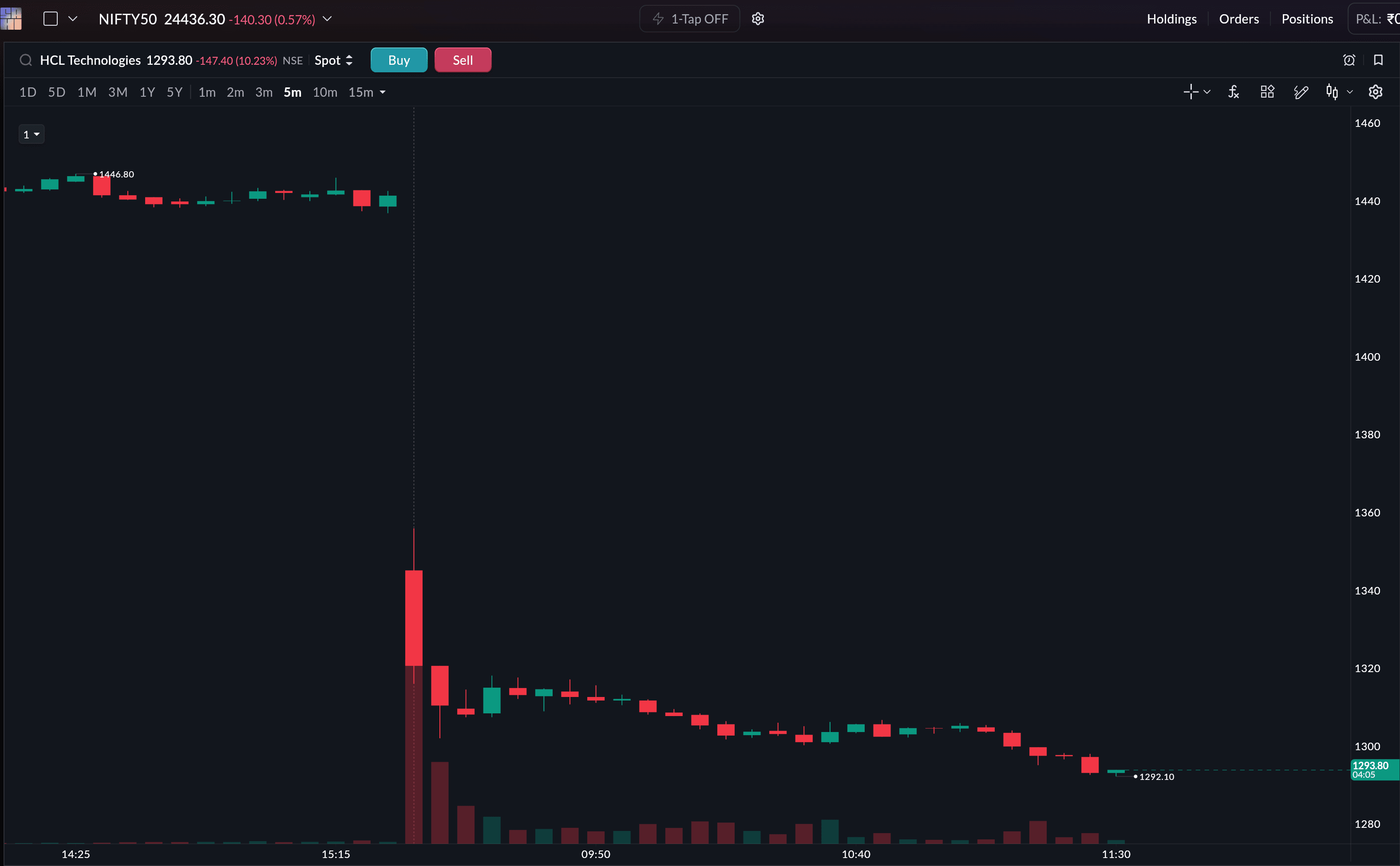

And yet, on Wednesday morning, HCL Tech's stock crashed over 9% on the NSE, opening at ₹1,345 against a previous close of ₹1,441. At one point, HCL Tech's share price touched ₹1,301 intraday, making it the top loser on the Nifty. Over the past week alone, the stock has shed more than 10%. (Stock price as of 11:30 am, 22nd April)

(Stock price as of 11:30 am, 22nd April)

So what on earth happened?

The Gap Between "Good" and "Good Enough"

Here's the thing about markets: they don't trade on results in isolation. They trade on results versus expectations.

Brokerages going into this quarter were expecting HCL Tech to report average net profits of around ₹4,716 crore and revenue of roughly ₹34,398 crore. What the company actually delivered — ₹4,488 crore in profit and ₹33,981 crore in revenue — fell short on both counts. In a market where analysts have already priced in a bullish scenario, even a small miss can trigger a sharp correction.

Think of it like a Bollywood film with sky-high advance bookings. If the opening weekend collection is merely "good" instead of "blockbuster," the stock of the production house tanks the next day. The film didn't fail. Expectations did.

That's exactly the trap HCL Tech walked into on Wednesday.

The Margin Story Nobody Wanted to Hear

Beyond the headline numbers, the detail that really stung investors was margin compression.

HCL Tech's EBIT (earnings before interest and taxes) came in at ₹5,620 crore for the quarter. While that's up 3.3% from a year ago, it's down a sharp 10.6% from the previous quarter's ₹6,285 crore. The EBIT margin, excluding restructuring costs, landed at approximately 17.7%, compared to around 18% a year ago and 18.6% in Q3 FY26.

That's a sequential contraction of roughly 90 basis points in margin. In plain language: HCL Technologies is earning less per rupee of revenue than it was just three months ago.

The culprits? A cocktail of pressures, seasonal decline in the high-margin HCL Software business, wage hikes that kicked in during the quarter, and restructuring expenses. The HCL Software segment, which includes software products, typically takes a hit in Q4 because of licensing cycles. But knowing why a margin falls doesn't make the fall hurt any less.

The Number That Scared Everyone: FY27 Guidance

If the Q4 numbers were disappointing, the FY27 guidance was the real gut punch.

Management guided for IT services revenue growth of just 1.5–4.5% in constant currency for FY27, with EBIT margins in the 17.5–18.5% band. Markets had been hoping for something bolder, especially given HCL Tech's aggressive AI deal wins and the $9,323 million in total contract value it secured across full-year FY26.

The guidance essentially tells investors: don't expect an acceleration. HCL Technologies is signaling caution about the macro environment, particularly the uncertainty around US tariffs, client spending, and global demand. With manufacturing and ER&D (Engineering Research & Development) verticals already under pressure from the slowdown in the auto sector and visibility on new revenue pools from GenAI still fuzzy, management chose to play it conservative.

Conservative guidance in uncertain times is prudent management. But in a market that was pricing in optimism, it felt like a cold shower.

What the Brokerages Are Saying

The analyst community's reaction to HCLTech earnings was swift and largely cautious.

Several brokerages downgraded or cut target prices on the stock, flagging "lower growth visibility" and trimming FY27–28 earnings estimates. One brokerage noted that at current valuations, HCL Technologies' share price trades at a premium to Infosys's FY27 consensus EPS, a premium that's hard to justify when growth is decelerating.

Others held their ground with a bullish stance. Their argument: free cash flow stood at approximately 111% of net profit for FY26; the company's diversified, infrastructure-heavy portfolio remains a structural positive even if near-term growth optics look murky.

Two very different reads from credible analysts. That alone tells you how much uncertainty is baked into this stock right now.

The Bigger Picture: IT Sector Under Pressure

HCL Tech isn't suffering in isolation. Wednesday also saw Infosys and TCS shares fall sharply, the entire Indian IT sector is grappling with the same headwinds. US clients are tightening budgets amid tariff-related uncertainty. Discretionary spending on tech transformation projects is being deferred. And while AI is creating new contract opportunities (HCL Tech's AI deal wins were a bright spot this quarter), it's also compressing revenue in areas like application maintenance, where AI-driven productivity reduces the hours billed.

This is the paradox of the AI era for IT services companies: the very technology they're selling is also disrupting their traditional billing model.

HCL Tech, to its credit, has been more proactive than peers in pivoting toward AI-led engagements. The $9,323 million in FY26 deal wins, including several advanced AI contracts, show the pipeline is healthy. But pipelines take time to convert into revenue. And in the short term, the market is paying attention to what's being delivered, not what's being signed.

So, Should You Be Worried?

That depends entirely on your time horizon.

If you're a short-term trader, the chart looks bleak, HCL tech share price is down roughly 15% from its January levels and has broken through several support levels. With muted near-term guidance and downgrades in the mix, there's no obvious near-term catalyst to reverse the momentum.

But zoom out to five years, and HCL Technologies has delivered north of 35% gains. The fundamentals — diversified revenue streams, strong deal wins, robust free cash flow (~111% of net profit for FY26), and a consistent dividend policy — haven't disappeared overnight.

The question investors need to ask isn't "did HCL Tech have a bad quarter?" (it didn't, really). The question is: "Is the market's current pessimism pricing in a worse future than what's actually likely to materialise?"

With the company generating free cash flow well above net profit and winning over $9 billion in deals annually, that's not an unreasonable thing to wonder.

That's all from us today. As always, this is not investment advice. Do your own research, consult a SEBI-registered advisor, and remember, stocks go up and down, but panic is always a choice.